If you live in Florida, you already know the sticker shock that comes with a home insurance bill. It’s not just a little more expensive than elsewhere—it’s in a completely different ballpark. The average premium for a standard home in the Sunshine State has climbed to a staggering $5,376 per year.

That number alone is enough to make you wince. But it’s the comparison to the rest of the country that truly highlights the financial pressure Florida homeowners are under.

Understanding Florida's High Insurance Premiums

Insuring a home here isn't just a simple transaction; it feels more like betting against the weather. While homeowners in other states pay to protect themselves from risks like fire or theft, Floridians are paying a massive premium for living in a place directly in the path of nature's most destructive storms.

This constant, elevated risk is the single biggest driver of our sky-high insurance costs.

The numbers don't lie. For a home with $300,000 in dwelling coverage, that $5,376 annual premium is more than double the national average of $2,181. This massive gap is fueled by Florida’s unique hurricane exposure and, frankly, a history of high litigation costs tied to insurance claims.

Florida vs. National Average at a Glance

Let's break that down with a simple, direct comparison to see just how wide the gap has become. It’s not a small difference; it’s a financial reality that reshapes household budgets across the state.

Florida Home Insurance Premiums at a Glance

| Metric | Florida Average | National Average |

|---|---|---|

| Annual Premium | $5,376 | $2,181 |

| Difference | +146% | Baseline |

This table tells the whole story. The financial burden is significant and sets Florida apart from the rest of the country. For a more in-depth look at what drives rates nationwide, check out our guide on the average cost of homeowners insurance.

This massive gap confirms a critical truth for anyone owning property here: Florida's insurance market plays by a totally different set of rules. Our state's geography and unique legal environment have created a perfect storm, resulting in the highest insurance costs in the nation.

Why Florida Home Insurance Rates Are So High

Trying to understand the average home insurance cost Florida residents face can feel like trying to solve a puzzle with missing pieces. It’s not just about the weather, though that’s a huge part of it. The sky-high premiums in the Sunshine State are the result of a perfect storm of powerful forces colliding, turning the market into a pressure cooker for homeowners' budgets.

The biggest driver is, without a doubt, catastrophic weather risk. Florida's geography makes it a magnet for hurricanes that are both frequent and incredibly powerful. Insurers have to game out the worst-case scenarios, using complex models to predict how many billions of dollars they’d need to pay out to rebuild homes and replace belongings after a monster storm.

This massive risk forces insurance companies to buy their own insurance, a safety net called reinsurance. Think of it as an insurance policy for the insurer. Because the potential losses in Florida are so immense, reinsurance is astronomically expensive, and that cost gets passed directly down to you in your premium.

The Impact of Litigation and Fraud

Beyond the wind and rain, Florida has been wrestling with a legal environment that’s been a nightmare for insurers. For years, the state was the epicenter of insurance lawsuits, with a wildly disproportionate number of claims ending up in court compared to the rest of the country.

This wasn't just homeowners fighting for fair payouts. The system was often exploited by contractors and attorneys, which sent the cost of claims into the stratosphere. A simple water leak could spiral into a full-blown legal war, with insurers paying far more in legal fees than it cost to fix the actual damage. Those inflated costs forced insurers to jack up rates for everyone just to stay afloat.

While recent laws have been passed to try and fix this, the financial scars from years of runaway lawsuits and fraudulent claims are still baked into the rates Floridians are paying right now. The market is still healing.

A Problem That Feeds on Itself

These issues don't happen in a vacuum—they fuel each other, making the whole situation worse.

- Frequent Storms: More hurricanes lead to more claims, putting constant financial stress on insurance companies.

- Inflated Claims: Widespread litigation meant even minor claims became excessively expensive, draining insurer reserves much faster than they should have.

- Rising Reinsurance Costs: As global reinsurers watched the massive payouts and legal battles in Florida, they hiked their own prices, adding yet another layer of cost.

This vicious cycle has made Florida an incredibly tough place for insurers to do business. Many smaller companies have gone broke, and several major national carriers have either pulled out of the state or drastically reduced how many homes they’ll cover.

Less competition means fewer choices and higher prices for you. To get a better handle on the specific coverages you need, you can learn more about why Florida homeowners need hurricane insurance in our detailed guide. It all adds up to create the high average home insurance cost Florida has become famous for.

Let's be blunt: Florida's home insurance market is a mess. For years, homeowners haven't just been battling sky-high premiums; they've been getting hit with non-renewal notices, leaving them scrambling to find anyone willing to cover their homes. It's created a constant state of anxiety for families across Florida.

The whole system was spiraling. Insurers were either going broke or packing up and leaving the state entirely. In response, state lawmakers finally stepped in with some massive legal reforms—think of it as them trying to hit a "market reset" button.

The big idea is to lure insurance companies back, spark some real competition, and eventually drive down the average home insurance cost Florida residents are forced to pay. But this kind of reset doesn't happen overnight. The market is still incredibly fragile.

The Rise of Non-Renewals and the Carrier Exodus

For a long time, the steady exit of insurance companies created a full-blown coverage crisis. As carriers fled, the few that remained got extremely picky, tightening their rules and dropping homes they decided were too risky. This is what caused that explosion of homeowners losing their policies.

This isn't just an inconvenience; it's a sign of a broken market. Florida homeowners have been living through a nightmare that saw a staggering 280% jump in non-renewals from 2018 to 2023—the highest spike in the entire country. In 2023 alone, Florida's non-renewal rate was 2.99%, miles ahead of the next-closest state. You can dig into the numbers yourself by reading the full report on Florida's home insurance non-renewal rates.

This left countless people with nowhere to turn for private insurance.

Can New Laws Actually Fix This?

To stop the bleeding, Florida passed some major laws aimed at fixing the root causes of the chaos. The main target? The endless, costly lawsuits that scared insurers away in the first place.

Here are the two biggest changes:

- Getting Rid of "One-Way Attorney Fees": This old rule meant insurers had to pay the homeowner's lawyer bills if they lost a lawsuit, but homeowners didn't have to pay the insurer's bills if they lost. It basically encouraged a flood of frivolous claims.

- Cracking Down on Assignment of Benefits (AOB): The new laws put a stop to contractors taking over a homeowner's insurance claim. That practice often led to ridiculously inflated repair bills and more lawsuits.

The whole point of these reforms is to make Florida a more predictable and stable place for insurance companies to do business. That's the first step to getting them to write more policies and actually compete for your business again.

The early signs are cautiously optimistic. We're seeing a few new insurance companies test the waters and a couple of existing ones are even starting to lower rates for the first time in ages. But let's be realistic—the road to a truly stable and affordable market is going to be a long one. Homeowners need to stay on their toes, but for the first time in a while, there's a glimmer of hope that the constant price hikes might finally start to slow down.

How Your Florida Location Impacts Your Premium

When it comes to the average home insurance cost Florida residents pay, one rule trumps all others: location, location, location. Where your home sits on the map is hands-down one of the biggest factors driving your premium. It's no exaggeration to say that moving just a few miles can mean a difference of thousands of dollars a year.

Insurers don't see Florida as a single market. They see a complex patchwork of risk zones, almost like a permanent weather map where some areas are always shaded red for high danger. The biggest variable? Proximity to the coast. Coastal properties simply bear the brunt of hurricane-force winds and catastrophic storm surges.

A home in an inland city like Gainesville is exposed to far less risk than one in a coastal hotspot like Miami-Dade County. This is the fundamental reason your premium can be so wildly different from your friend's, even if your houses are the same size and value.

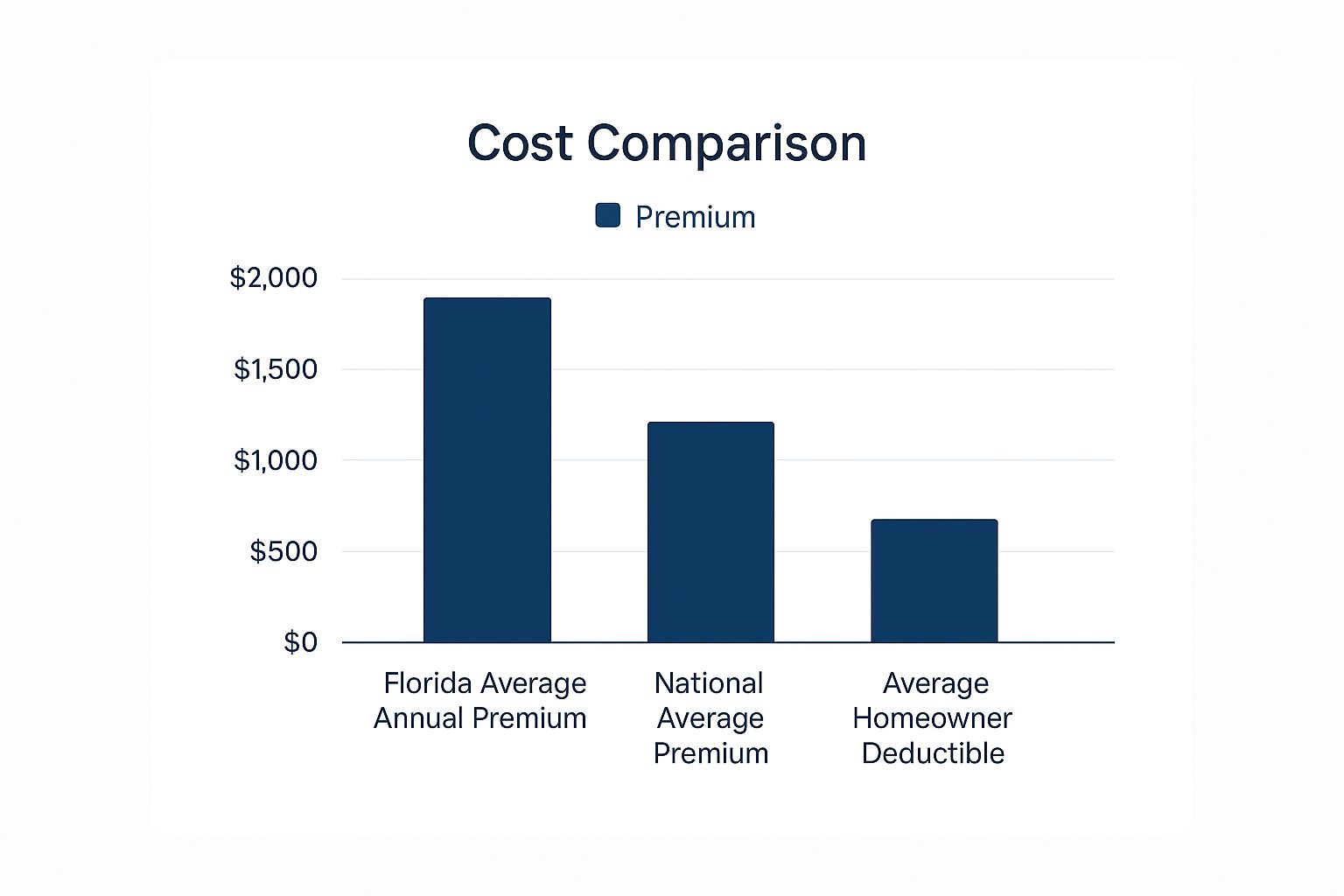

This image really puts the financial impact of Florida's geography into perspective, showing how our state's average premium stacks up against the rest of the country.

As you can see, the average premium in Florida is dramatically higher than the national figure. That gap is almost entirely explained by the state's unique and severe weather risks.

City-by-City Cost Breakdown

Let’s turn this from an abstract idea into real dollars and cents. The difference in premiums between a high-risk coastal city and a lower-risk inland one is stark. Insurers use incredibly sophisticated models to predict the odds of a major storm hitting a specific zip code, and they price their policies based on those calculations.

Your premium is a direct reflection of your home's calculated risk. If you live in an area that historical data and predictive models flag as a likely target for future storms, your rate will be higher—no matter how well-built your house is.

To give you a clear snapshot of how geography directly hits your wallet, here’s a look at estimated annual premiums for a home with $300,000 in dwelling coverage across several Florida cities.

Average Home Insurance Costs by Florida City

| City | Estimated Annual Premium | Risk Factor (Coastal/Inland) |

|---|---|---|

| Miami | $8,750 | High-Risk Coastal |

| Fort Lauderdale | $7,900 | High-Risk Coastal |

| Tampa | $5,200 | Moderate-Risk Coastal |

| Orlando | $4,100 | Moderate-Risk Inland |

| Gainesville | $2,950 | Lower-Risk Inland |

The numbers don't lie. Moving just a hundred miles inland can literally cut your insurance bill by more than half. Understanding your home's specific, location-based risk is the first real step to making sense of your policy's cost.

Key Factors That Drive Your Personal Rate

While your zip code sets the stage, it's the specific details of your home that really dial in your final premium. The average home insurance cost Florida provides a baseline, but insurers dig much, much deeper. Think of it less like a flat rate and more like a personalized risk assessment for your specific property.

Every detail, from the materials used to build your house to the age of its roof, helps an underwriter build a complete picture. This is exactly why two next-door neighbors can get wildly different quotes. Your home's individual characteristics are just as important—if not more so—than its location on the map.

Your Home's Structural DNA

The physical makeup of your house is a huge deal for any Florida insurer. They're laser-focused on one big question: how will this home stand up to hurricane-force winds?

- Construction Type: A home built with concrete block is seen as far more resilient than a wood-frame structure. That single detail can lead to some serious savings because concrete is simply better at resisting both wind and the debris it throws around.

- Home Age: Older homes often come with outdated building codes, wiring, and plumbing. This makes them more vulnerable to all sorts of damage, especially from storms. A newer home built to modern hurricane standards will almost always be cheaper to insure.

Your roof is arguably the single most critical component an insurer looks at. Its age, material, and even its shape can dramatically swing your premium, since it's your home's first line of defense against severe weather.

A roof older than 15 years can make it tough—and expensive—to find coverage at all. Insurers see it as a major liability just waiting to fail. The shape also matters immensely. A hip roof, which slopes down on all four sides, is more aerodynamic and performs much better in high winds than a standard gable roof, often earning you a substantial discount.

Personal and Protective Factors

Beyond the nuts and bolts of the structure, insurers look at your personal history and the protective measures you've put in place. These elements help them figure out your individual risk level.

Your personal claims history is a big one. Filing multiple claims in a short time, even for small things, can flag you as a higher risk and push your rates up. On the flip side, insurers love to reward homeowners who have a clean, claim-free record.

Finally, being proactive really pays off. Installing wind mitigation features—things like hurricane shutters, impact-resistant windows, and a reinforced garage door—shows you're serious about protecting your property. These upgrades can unlock some of the biggest discounts available, directly lowering the average home insurance cost Florida homeowners have to face.

Actionable Steps to Lower Your Insurance Bill

When you see your Florida home insurance bill climb, it's easy to feel like you're stuck. But you have more power to lower that premium than you might think. Even in this crazy market, taking a proactive stance can lead to some serious savings.

The trick is to stop worrying about the things you can't change—like hurricane season—and start focusing on the things you can. It’s all about playing offense with your home's resilience and your insurance choices.

Fortify Your Home for Major Discounts

One of the smartest moves a Florida homeowner can make is investing in wind mitigation. This just means strengthening your home against the brutal force of hurricane winds. Think of it like preventative medicine for your house; the stronger it is, the less risky it looks to an insurer, and that translates directly into discounts for you.

These features can unlock some of the biggest savings on your policy:

- Hurricane Shutters: Installing approved storm shutters or impact-resistant windows is a huge win.

- Reinforced Garage Doors: Your garage door is often the weakest link in a major storm. Beefing it up is critical.

- A Hip Roof: A roof that slopes down on all four sides is far more aerodynamic and wind-resistant than a standard gable roof.

- Strong Roof-to-Wall Connections: This means using hurricane clips or straps to literally tie your roof trusses to the walls, adding incredible structural strength.

Once you’ve made these upgrades, you must get a certified wind mitigation inspection. That official report is your golden ticket—it proves your home’s strength to the insurance company and forces them to give you the discounts you've earned.

The savings from a thorough wind mitigation inspection can be substantial. In many cases, the lower premium in the very first year more than pays for the inspection itself. It's a direct investment in cutting your long-term insurance costs.

Smart Policy and Shopping Strategies

Beyond physical upgrades, the way you manage your policy and shop for coverage makes a massive difference. Don't just blindly accept your renewal notice when it arrives in the mail each year.

First up, consider raising your deductible. Your deductible is what you pay out-of-pocket on a claim before your insurance kicks in. Bumping it up from, say, $1,000 to $2,500, means you’re taking on a bit more of the initial risk, but it can lower your annual premium right away.

Next, look into bundling your home and auto policies. Most carriers will give you a pretty hefty discount—often 10% or more—just for keeping both policies with them.

Finally, and this is the most important one: shop around every single year. The Florida insurance market is always in flux. The company that gave you the best deal last year probably isn't the most competitive one this year. If you're ready to find a better rate, our guide on how to switch insurance companies lays out the process step-by-step. In today’s market, loyalty rarely pays off—but diligence always does.

Common Questions About Florida Home Insurance

Trying to make sense of Florida's home insurance market can feel like navigating a maze in the dark. Even when you get a handle on the basics, the rules seem to change constantly. Here are some of the most common questions we hear, with straight-up answers.

Why Did My Rate Increase Without Any Claims?

It’s probably the most frustrating call a Florida homeowner has to make: "I've never filed a claim, so why did my premium just skyrocket?" The simple, maddening answer is that your personal track record is only a tiny piece of a much larger puzzle.

Insurers don't just set your rate based on you. They set it based on the entire state.

Your premium is getting pushed up by forces totally out of your control. Think of things like the soaring cost of reinsurance (the insurance that insurance companies have to buy), the insane price of lumber and labor needed for storm repairs, and new hurricane models that predict a tougher future for your whole region. You're not just paying for your own risk; you're paying for the collective risk of insuring any home in Florida.

Your rate isn't just about your house. It’s a reflection of the massive, shared expense of operating in the Sunshine State.

Is a Wind Mitigation Inspection Worth The Cost?

In a word: absolutely. A wind mitigation inspection isn't just a good idea in Florida—it's one of the most powerful tools you have to directly slash your insurance bill. Think of it less as an expense and more as a strategic investment with a fast payoff.

A certified inspector comes to your home and documents all the features that make it tougher against hurricane-force winds. This could include things like:

- A hip roof design, which is naturally more aerodynamic.

- Hurricane clips or straps that anchor your roof to the walls.

- Impact-resistant windows or approved storm shutters.

- A reinforced garage door to prevent it from blowing in.

Having these features documented can unlock some of the biggest discounts available on your policy, many of which are required by Florida law. It’s not uncommon for the savings in the first year alone to be more than the cost of the inspection itself.

What if No Private Insurer Will Cover Me?

Getting turned down by private insurance companies doesn't mean you're out of luck. Florida created a state-backed, non-profit company called Citizens Property Insurance Corporation for this exact situation. It acts as the "insurer of last resort" for residents who can't find a policy anywhere else.

While Citizens is an essential safety net, it's not meant to be a permanent home. Its coverage can be more limited, and its rates are intentionally designed to be higher than private market options. This is done on purpose to encourage homeowners to find a private policy as soon as one becomes available.

Finding the right coverage at a price that makes sense is a huge challenge, but you don’t have to tackle it alone. The experts at MyEasyRate Insurance are here to help you compare quotes from multiple companies to find the best fit for your home and budget. Visit us online to get a free quote today!