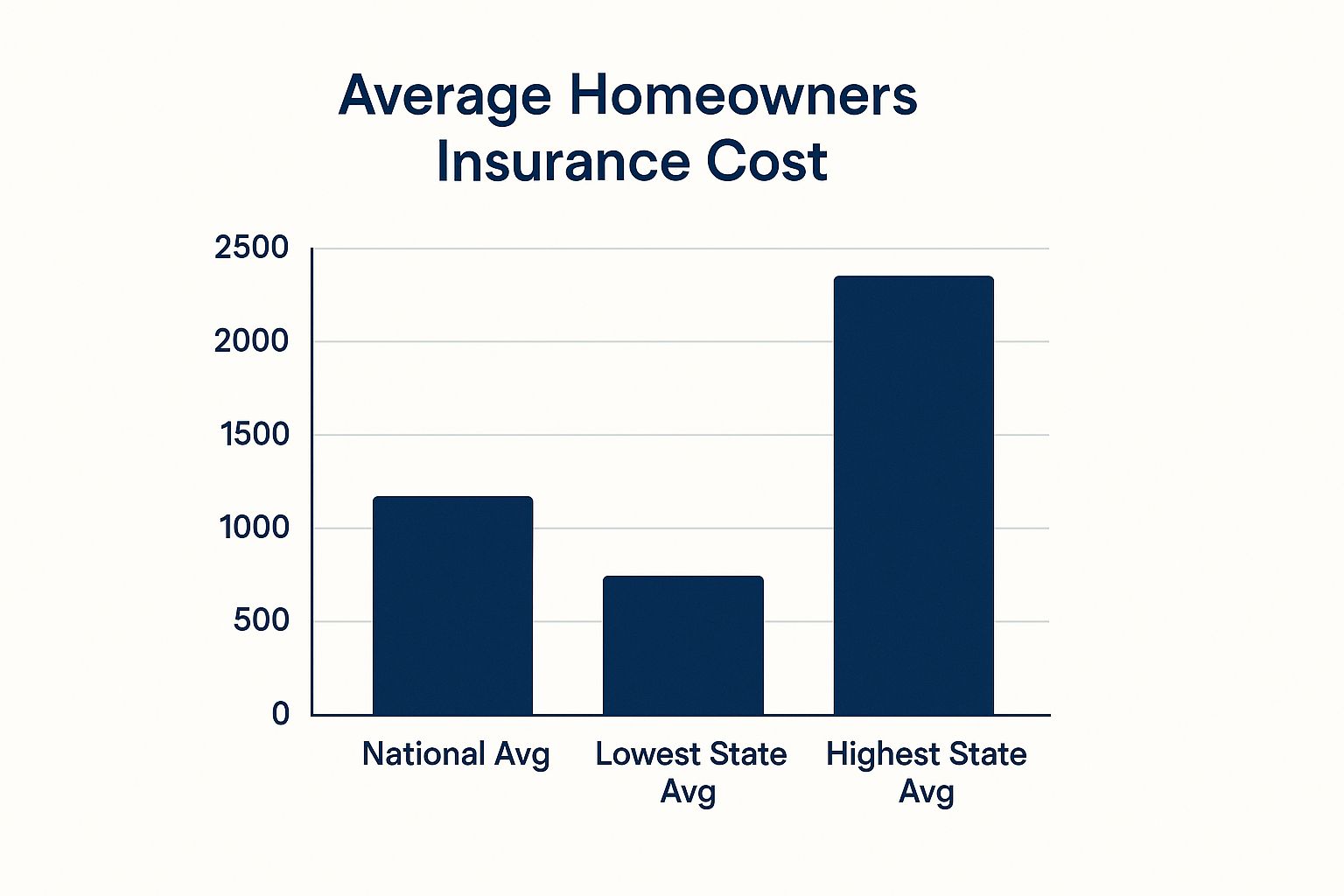

If you've started shopping for homeowners insurance, you've probably seen a few headline numbers floating around. For 2025, the average cost of homeowners insurance is projected to be about $3,520 per year. But that number is just a national benchmark—a starting point, not a price tag.

The actual price you'll pay is a highly personalized figure. Think of it less like a sticker price at a store and more like a custom-tailored suit, designed to fit the unique risks and features of your specific property.

The Real Cost of Protecting Your Home

Understanding the "average" cost is the first step, but it doesn't tell the whole story. Your insurance premium is a dynamic financial shield built just for your home, and the cost of that shield depends on dozens of factors.

This is why your neighbor, living just a few doors down in a similar house, might have a completely different insurance bill. Their home's age, the type of roof they have, their claims history—it all gets factored into their final rate.

What's Driving Up the National Average?

So, why are the numbers climbing? The national average is heavily influenced by broader market forces, especially the growing frequency and intensity of severe weather events.

That projected 8% increase in premiums for 2025 is largely driven by the fallout from hurricanes along the Gulf Coast, which happens to be home to some of the most expensive insurance markets in the country. To see how these regional risks are shaping costs for everyone, you can dive deeper into these home insurance price projections.

These big-picture trends mean that even if you've never filed a claim and live in a low-risk area, your rates can still rise. To get a real grip on what you’ll pay, you have to look past the average and focus on the specific variables insurers use to size up your property.

Here are the big four:

- Your Home's Location: Are you near a coastline? A wildfire zone? How close is the nearest fire hydrant or station? Geography is everything.

- Property Characteristics: The age of your home, its construction materials (brick vs. wood frame), and the condition of major systems like the roof and electrical panel all matter. A lot.

- Coverage Choices: How much protection do you want? The limits you choose for your dwelling, personal property, and liability directly impact your premium.

- Your Personal Profile: Your claims history is a major factor. In some states, your credit-based insurance score also plays a role.

Once you see how these pieces fit together, it becomes clear why the "average cost" is just a conversation starter, not the final answer.

A Look at State-by-State Differences

Nothing highlights the impact of location better than looking at costs across state lines. Below is a snapshot of estimated average annual premiums in some of the highest-cost and lowest-cost states, showing just how dramatic the difference can be.

Average Homeowners Insurance Costs by State

| State | Projected Average Annual Premium | Primary Risk Factor |

|---|---|---|

| Oklahoma | $5,400 | Tornadoes & Hail |

| Nebraska | $5,350 | Severe Storms & Hail |

| Florida | $4,900 | Hurricanes & Flooding |

| Texas | $4,750 | Hurricanes, Hail & Wildfires |

| Delaware | $1,100 | Low |

| Vermont | $1,150 | Low |

| New Hampshire | $1,200 | Low |

| Oregon | $1,250 | Relatively Low (Wildfire risk rising) |

Source: Projections based on 2024 market analysis and forward-looking risk models.

As you can see, states hammered by recurring natural disasters like hurricanes and tornadoes face dramatically higher costs than states with milder weather patterns. This is the clearest illustration of risk in action.

Why Home Insurance Premiums Are Rising

If you just opened your latest home insurance bill and felt a jolt of sticker shock, you’re definitely not alone. Homeowners across the country are watching their premiums climb, but it’s not just a random price hike. There are some powerful, interconnected forces pushing the average cost of homeowners insurance up.

When you understand what’s happening behind the scenes, the increases start to feel less arbitrary. The two biggest drivers are the skyrocketing cost of rebuilding a home and the relentless increase in costly natural disasters. When those two problems hit at the same time, the entire insurance market feels the squeeze.

The Soaring Cost of Rebuilding

At its heart, home insurance is a simple promise: if a covered disaster hits, your insurer will pay to repair or rebuild your house. But what happens when the cost of keeping that promise doubles? That’s exactly what we’re seeing, as inflation has hammered construction materials and labor costs.

Just think about the basic ingredients of a house—lumber, shingles, drywall, and copper wiring. The prices for these essentials have surged over the past few years. This means if your home were to burn down today, it would cost an insurance company far more to rebuild it to the same standard than it would have just a few years ago.

Key Takeaway: When the cost to rebuild a home goes up, the cost to insure that home has to follow. Insurers have to adjust their premiums to make sure they have enough cash on hand to cover these much larger potential claim payouts.

It’s not just materials, either. A persistent shortage of skilled construction workers also means higher wages and longer project timelines, adding another layer of expense to any claim.

The Growing Threat of Severe Weather

The other major force cranking up premiums is the undeniable uptick in severe weather events. From destructive wildfires out West to powerful hurricanes in the Southeast and massive hail storms across the Midwest, insurers are paying out more claims, more often.

Each of these catastrophes can trigger billions of dollars in insured losses. To protect themselves from that kind of massive risk, insurance companies buy their own insurance, a product called reinsurance. When these global reinsurers get hit with huge payouts from disasters all over the world, they raise their rates.

This kicks off a chain reaction. Higher reinsurance costs get passed down to your local insurance company, which then has to pass those costs on to you in the form of higher premiums. This problem has gotten so bad in high-risk states that some insurers have decided to stop offering coverage there altogether. You can learn more about what happens when major insurers leaving a state impacts homeowners and shakes up the local market.

And this trend isn't slowing down. Market data shows a clear pattern of acceleration. The average premium for new home policies jumped 9.3% between 2024 and 2025, which came right after an even bigger increase of 18.8% the year before. You can dive deeper into these recent insurance market trends to see the full picture.

Decoding Your Home Insurance Rate

This graphic from the Insurance Information Institute lays out the core ingredients that an insurer mixes together to cook up your final premium. As you can see, it’s about a lot more than just your home’s price tag—everything from the local fire department's response time to the deductible you choose gets factored in.

Your Home’s Unique Profile

Think of your house as having its own risk profile, sort of like a personal health record. An insurer’s job is to read that profile and guess how likely you are to file a claim down the road. The more risk they see, the higher your premium will be. Simple as that.

A few key characteristics of your property play a starring role in this evaluation.

First up is the construction material. It's just common sense: a brick or masonry home stands up to fire better than a wood-frame house, and that resilience often earns you a lower premium. The age of your home is another huge one. Older homes can have aging electrical or plumbing systems, which are ticking time bombs for fire or water damage in an insurer's eyes.

Your roof's condition is also front and center. A new, solid roof is your home's first line of defense against Mother Nature, so insurers are more than happy to reward homeowners who invest in a sturdy, modern roof with better rates.

Protective Features and Safety Measures

Next, insurers zoom in on the safety gear you have installed. These are the proactive steps you’ve taken to cut down the odds of a disaster, and they often translate directly into discounts on your policy.

Installing a few protective devices can make a real difference in what you pay. Insurers love to see features that tackle common risks head-on.

- Smoke Detectors: Pretty much every home has them, but systems that are centrally monitored give you a bigger safety net and, in turn, a bigger discount.

- Home Security Systems: If your system automatically calls the police or fire department during a break-in or fire, you've just made your home a much safer bet.

- Fire Sprinklers: While not as common in single-family homes, they offer top-tier fire protection and can lead to some of the most substantial savings.

- Water Leak Detectors: These smart gadgets that shut off the water main the second they detect a leak are getting popular for a reason—they stop costly water damage claims before they start.

Even something as simple as your home’s address matters. Being close to a fire station or a hydrant means a fire will likely be put out faster, limiting the damage. That’s a risk reduction an insurer can quantify.

A home located within five miles of a fire station and within 1,000 feet of a fire hydrant is typically viewed much more favorably by insurers. This proximity directly translates to a lower calculated risk and, consequently, a lower cost for your coverage.

Your Personal Underwriting Factors

Finally, it gets personal. Insurers look at your past behavior to predict your future actions, and this goes beyond just the four walls of your house.

Your claims history is one of the heaviest hitters. If you’ve filed a few claims in the past couple of years, an insurer is going to see you as a higher risk and charge accordingly. This is exactly why it's often smarter to pay for minor repairs yourself instead of filing a small claim.

On top of that, most states allow insurers to use a credit-based insurance score. It’s not the same as your regular credit score, but it’s built from your credit history. Years of data have shown a clear link between this score and the likelihood of someone filing a claim. So, a solid credit history can often lead directly to a lower homeowners insurance bill.

How Your ZIP Code Shapes Your Premium

When it comes to the average cost of homeowners insurance, your home’s address is the single most important line item on the application. Forget your credit score or the age of your roof for a second. While those things matter, nothing moves the needle on your premium quite like your specific location. An insurer’s first question is always "where," because geography dictates risk.

Think of it this way: insuring a home is like placing a bet on its safety. A house in a quiet, inland area with mild weather and low crime is a pretty safe bet. But a home on a hurricane-prone coastline or in a wildfire corridor? That’s a much higher-stakes wager, and the premium is going to reflect that elevated risk.

This infographic shows just how dramatically the average cost can swing from one state to another based purely on those local risks.

As you can see, a "national average" is just a statistical midpoint. The reality on the ground for your policy can be thousands of dollars higher or lower.

From State Lines to Street Signs

Insurers drill down much further than just your state. They analyze risk at the ZIP code level and even by the neighborhood. Two homes just a few miles apart can have surprisingly different rates if one sits in a floodplain or has a higher local crime rate.

This hyperlocal focus is why homeowners in states like Florida, Texas, and Colorado often see some of the nation’s highest insurance bills. These regions are ground zero for specific, recurring disasters:

- Hurricanes and Windstorms: Coastal areas from Texas to Florida face a constant barrage, leading to massive, widespread claim events.

- Hail and Tornadoes: "Tornado Alley" and much of the Midwest are hotspots for severe storms that shred roofs and siding, causing billions in damage.

- Wildfires: Western states are increasingly exposed to wildfire risk, which can wipe out entire communities in a single event.

To see how this plays out, we can look at a few examples of how regional climate risk directly impacts your insurance bill.

Cost Drivers by Regional Risk

| Region | Primary Climate Risk | Impact on Insurance Premiums |

|---|---|---|

| Florida & Gulf Coast | Hurricanes | Extremely high wind/hail deductibles (often 2-5% of home value); some insurers have stopped writing new policies entirely. |

| California & Colorado | Wildfires | High premiums in high-risk zones (WUI areas); insurers are non-renewing policies and requiring extensive mitigation efforts. |

| Texas & Oklahoma | Hail & Tornadoes | Some of the highest average premiums in the US due to the sheer frequency of severe storm claims for roof and siding damage. |

| Midwest & Plains | Convective Storms | Rising rates due to the increasing severity of hail, wind, and tornadoes, even outside of traditional "Tornado Alley." |

This table makes it clear: where you live determines what you’re up against, and insurance companies price their policies accordingly.

An insurer's view of your home's risk even includes its immediate surroundings. Your proximity to a fire station and the nearest fire hydrant are calculated into your rate. Why? A faster emergency response time can dramatically reduce the severity of a claim.

The financial impact of these localized risks is staggering. A recent government analysis found that between 2018 and 2022, homeowners insurance premiums shot up 8.7% faster than general inflation, driven almost entirely by climate-related damages. The report also highlights that while costs went up everywhere, the increases varied immensely by region and ZIP code. You can dig into the findings on localized insurance costs for more detail.

Ultimately, your location sets the baseline for your premium. While you can’t exactly move your house, understanding your local risks explains why your rate is what it is—and why shopping for the right coverage is a uniquely local experience.

Practical Ways to Lower Your Home Insurance

Knowing what drives your premium is one thing, but actually getting it to drop is another. You can't just pick up your house and move it to avoid hurricanes, but you absolutely have a say in other parts of the insurance equation. Taking control can lead to some serious savings on your annual bill.

The trick is to start thinking like an insurer. Your whole goal is to make your home look like a safer, less risky bet. Every step you take to lower the odds of a claim—whether it's from a break-in, a kitchen fire, or a burst pipe—can translate directly into a discount.

Bundle Your Policies for an Easy Win

One of the simplest and most effective ways to cut your home insurance cost is to bundle your policies. This just means buying your home and auto insurance from the same company. Insurers love it when you do this—it builds loyalty, gives them more business, and they'll happily reward you with a hefty discount.

Bundling can often knock 10% to 25% off your combined premiums. It's a no-brainer strategy that takes almost no effort but pays off year after year. If you've got policies with different carriers right now, getting a bundled quote should be your first move.

Increase Your Deductible Strategically

Your deductible is simply the amount you agree to pay out-of-pocket before your insurance coverage kicks in. If you choose a higher deductible, you're telling the insurance company you're willing to handle more of the small stuff yourself. In return, they'll lower your premium.

Think of it this way: A higher deductible signals to your insurer that you aren't likely to file piddly little claims for minor issues. This saves them a ton in administrative costs and potential payouts, and they pass a piece of that savings on to you.

For example, just bumping your deductible from $500 to $1,000 could slice your premium by as much as 20%. The key is to pick an amount you could comfortably pay tomorrow without breaking a sweat. It's a balancing act between lower monthly payments and what you have in your emergency fund. This is a very different lever than other property expenses; for instance, you can learn more about how homeowners can reduce property taxes to see how different savings strategies work.

Invest in Home Safety and Security

Making your home a tougher target for thieves and more resilient against common hazards is a direct path to lower insurance costs. Insurers offer a whole menu of discounts for features that reduce the risk of fire, theft, and water damage.

- Install a Security System: A monitored alarm system that automatically calls the police or fire department can trim your premium by 5% to 15%.

- Upgrade Smoke and CO Detectors: Modern, hardwired smoke and carbon monoxide detectors that are all connected offer better protection, and insurers often reward that with a small discount.

- Add Water Leak Sensors: These gadgets are becoming a huge deal. Automatic water shut-off devices can stop a small leak from turning into a catastrophic flood—one of the biggest sources of claims—and many insurers now offer nice discounts for them.

Maintain a Good Credit Score

In most states, your credit history plays a role. Insurers use something called a credit-based insurance score to help predict how likely you are to file a claim. Statistically speaking, people who manage their finances well also tend to file fewer claims.

By keeping up a solid credit history—paying your bills on time, keeping debt in check—you can directly improve your insurance score. Over time, this can lead to a lower average cost of homeowners insurance, rewarding your financial discipline with real savings on your policy.

Shopping Around for a Better Home Insurance Policy

Finding the right home insurance isn't just about chasing the lowest price—it's about getting the best possible value to protect what is likely your biggest asset. The average cost of homeowners insurance can swing wildly from one company to the next, even for the exact same house. That’s why grabbing the first quote you see is one of the biggest mistakes you can make.

To really nail down the best deal, you have to pit multiple carriers against each other. Most experts will tell you to get at least three to five quotes before you even think about making a decision. This is the only way to see which insurers like the look of your home's risk profile and are willing to offer the most competitive rates to win your business.

How to Make a True Apples-to-Apples Comparison

When the quotes start rolling in, your eyes will naturally jump to the final premium. But hold on. A cheap policy is no bargain if it leaves you high and dry after a disaster. To compare your options fairly, you need to line up the core components of each policy side-by-side.

Use this quick checklist to make sure you're looking at equivalent coverage:

- Dwelling Coverage (Coverage A): Are the limits the same on every quote? This number needs to be high enough to rebuild your home from scratch if it were a total loss.

- Personal Property (Coverage C): Check the coverage amount. More importantly, is it for actual cash value (which pays what your stuff is worth today) or the much better replacement cost (which pays to buy new items)?

- Liability Protection (Coverage E): Make sure the liability limits are identical. This coverage is what protects your entire financial future if someone gets hurt on your property.

- Deductibles: Are the deductibles the same for both standard claims (like a fire) and special perils (like wind or hail)? A low premium can easily hide a dangerously high deductible you'd struggle to pay.

Looking Beyond the Price Tag

The cheapest policy on the market is worthless if the company ghosts you when you need them most. Before you sign anything, spend a few minutes digging into the insurer's reputation. A company's track record is just as important as the premium it charges you.

Pro Tip: Look up an insurer’s financial strength rating from an agency like AM Best. A high rating (think A or better) is a strong signal that the company is on solid financial ground and can actually pay its claims, even after a massive catastrophe.

You should also hunt for customer service reviews and claims satisfaction scores from independent sources. Hearing from real policyholders gives you the inside scoop on how a company really operates—how they handle claims, communicate with customers, and resolve problems. Choosing an insurer known for both financial stability and great service brings a peace of mind that saving a few bucks a month just can't buy.

A Few Final Questions About Home Insurance Costs

To wrap things up, let's hit a few of the most common questions homeowners ask when they're trying to get a handle on the average cost of homeowners insurance. Getting these answers straight can clear up a lot of confusion and save you money down the road.

How Often Should I Actually Shop for New Home Insurance?

It's a really smart habit to review your policy and compare quotes at least once a year. Your life isn't static, and neither is your home—big changes can unlock some serious savings.

For instance, did you finish a major renovation, put on a brand-new roof, or even see your credit score jump up? Any of those events could qualify you for a much better rate. Shopping around annually makes sure your current insurer is still giving you a competitive price for the coverage you have, and that you haven't outgrown your policy.

Will Filing a Small Claim Really Increase My Premium?

Yes, in almost every case, it absolutely will. Filing a claim—even a small one—tells your insurer you're a higher risk to cover. That often triggers a rate increase when your policy renews. That surcharge can stick around for several years, easily costing you more in the long run than the original claim was even worth.

A good rule of thumb is to only file claims for major, catastrophic damage that blows way past your deductible. For the smaller stuff, it's almost always cheaper to pay out-of-pocket and protect your claims-free discount.

Why Did My Premium Go Up if I Never Filed a Claim?

This is one of the most frustrating things a homeowner can experience, but it's incredibly common. Your premium can climb even with a perfect claims record because of broad, external factors that are completely out of your control.

These factors often include:

- Widespread inflation that drives up the cost of lumber, shingles, and labor, making any potential repair more expensive for the insurance company.

- An increase in severe weather events in your region. If hurricanes, wildfires, or hailstorms become more frequent nearby, insurers adjust rates for everyone in the area to cover their higher expected losses.

- General rate adjustments made by your insurer to stay profitable after a costly year across their entire book of business.

And a quick note for renters—while this guide focuses on homeowners, you face similar risks to your personal belongings. It’s important to understand your options, and you can learn more about protecting your belongings with renters insurance in our detailed guide.

Ready to see if you can find a better rate for your home insurance? The team at MyEasyRate Insurance is here to help you compare quotes from top carriers to find the perfect balance of coverage and cost. Get your free, no-obligation quote today at https://myeasyrate.com.

Article created using Outrank