You’ve probably heard the term "umbrella insurance," but what does it actually do? Think of it less like a standalone policy and more like a massive upgrade to the liability protection you already have.

It's an extra layer of coverage that sits on top of your existing home and auto insurance, kicking in only after you've maxed out those policies. In short, it’s the financial backstop for when things go really, really wrong.

Understanding Umbrella Insurance And How It Works

Imagine your homeowners or auto insurance as your first line of defense. They have specific limits on how much they'll pay if you're found liable for someone else's injuries or property damage. But what happens if a serious car accident leads to a lawsuit that blows past your policy's limit?

This is exactly where umbrella insurance steps in.

It works by adding a much higher limit—typically starting at $1 million—on top of what you already have. If a catastrophic claim exhausts your auto policy's $300,000 liability limit, your umbrella policy would activate to cover the rest, up to its own much larger limit. This simple function can prevent you from having to drain your savings or sell assets to pay a massive legal judgment.

A Financial Safety Net

At its core, this policy is a form of excess liability coverage designed to protect your assets and future earnings from being seized after a lawsuit. Without it, your savings, investments, and even your home could be on the line.

And the best part? It’s surprisingly affordable for the peace of mind it delivers. The first $1 million in umbrella coverage typically costs between $150 and $300 a year. You can get more insights on umbrella insurance costs from Farmers.com.

Key Takeaway: An umbrella policy doesn’t replace your primary insurance. It enhances it by providing high-limit protection for those worst-case-scenario events that could otherwise lead to financial ruin.

Here’s a quick breakdown of what an umbrella policy really does for you.

Key Functions of Umbrella Insurance at a Glance

This table simplifies the main jobs of an umbrella policy.

| Function | Explanation |

|---|---|

| Increases Liability Limits | Adds a big layer of protection (e.g., $1M+) on top of your existing policies. |

| Covers Catastrophic Events | Protects you from major lawsuits or claims that exceed standard coverage. |

| Protects Your Assets | Safeguards your home, savings, and future income from legal judgments. |

Ultimately, it's a powerful tool for shielding the life you've worked hard to build.

What an Umbrella Policy Actually Covers

Think of an umbrella policy as a second layer of defense for your finances. It does two critical things that your standard insurance just can't: it provides excess liability coverage, and it steps in to cover bizarre claims your other policies won't even touch.

Its most common job is to act as a massive safety net. When a major claim completely drains the limits of your auto or homeowners policy, the umbrella policy kicks in. It’s the difference between a terrible accident and total financial ruin.

Extending Your Standard Liability Limits

The core function here is simple: when your regular insurance runs out, your umbrella policy takes over.

Let's say you're found at fault in a serious car accident, and the damages total $500,000. Your auto insurance is pretty good, but it maxes out at $300,000. Where does the other $200,000 come from? Without an umbrella policy, it comes straight out of your savings, your home equity, or your future wages. With one, the umbrella policy pays that remaining balance. You can see more on this at AmFam.com.

And this isn't just for car wrecks. It applies to your home, too, covering those nightmare scenarios:

- A delivery person takes a bad fall on your icy front steps, resulting in a massive lawsuit.

- Your friendly dog has a bad day and bites a neighbor, leading to expensive medical bills.

- A dead tree on your property crashes down onto your neighbor's brand-new garage.

Covering Personal Injury and Other Unique Claims

This is where umbrella insurance gets really interesting. It covers claims that standard policies almost always exclude, specifically those involving personal injury—and we’re not talking about broken bones. We're talking about damage to someone's reputation or character.

Key Insight: Standard policies are built for bodily injury and property damage. An umbrella policy goes further, often covering claims like libel (written defamation), slander (spoken defamation), false arrest, and malicious prosecution.

Imagine you post a scathing online review of a local contractor that leads to a defamation lawsuit. Your homeowners policy won't help, but your umbrella policy could cover the legal fees and any judgment against you.

This kind of protection is also a lifesaver for landlords, who face unique liability risks similar to those we touch on in our guide on why renters insurance matters. At the end of the day, it's designed to fill the most dangerous gaps your primary insurance policies leave behind.

Real-World Scenarios Where Umbrella Insurance Protects You

It’s one thing to talk about liability limits, but the real value of umbrella insurance clicks when you see it in action. Lawsuits can pop up from the most ordinary situations, and the costs can spiral far beyond what your standard auto or home insurance policies will cover.

Let's walk through a few scenarios where this extra layer of protection isn't just a nice-to-have—it's the only thing standing between you and financial ruin.

Imagine you're driving and cause a serious multi-car pile-up. After the dust settles, a court awards the injured parties a judgment of $800,000. Your auto insurance policy has a liability limit of $300,000, which is a pretty standard amount. That leaves you personally on the hook for the remaining $500,000.

Without an umbrella policy, that half-million-dollar gap could mean losing your house, your retirement savings, and even having your future wages garnished. With one? The umbrella policy kicks in and covers that difference, protecting everything you've worked for.

Beyond the Driver's Seat

The risks don't end when you pull into your driveway. Your own property can become the scene of a life-altering liability claim.

Think about a classic backyard barbecue. A guest slips on a wet spot on your patio and suffers a severe injury that requires major surgery and ongoing physical therapy. The total damages, including medical bills and lost wages, come out to $1 million.

Your homeowners insurance covers the first $500,000, but you're now responsible for the other half. Once again, a personal umbrella policy would step in to cover that excess amount, shielding your assets from being liquidated to pay the debt. This is especially true in states prone to unique risks; for instance, understanding why you need hurricane insurance for Florida homeowners shows how regional factors can create unexpected liabilities.

Protection for Modern Problems

Umbrella coverage is also great because it often extends to personal injury claims that your standard policies won't touch, like libel or slander.

Example: You leave a scathing online review for a local contractor. The business owner sues you for libel, arguing your post destroyed their reputation and cost them business. The court agrees and awards them a $150,000 judgment. Your homeowners policy almost certainly excludes this kind of claim. An umbrella policy, however, could be your only defense, covering both your legal fees and the final judgment.

These examples make it clear: umbrella insurance is far more than just another policy. It’s a critical safeguard for your financial future.

How Much You Should Expect to Pay

With all this talk of million-dollar liability shields, you’d think umbrella insurance would break the bank. But here's the surprising truth: it's one of the best bargains in the insurance world.

For the first $1 million in coverage, most people pay somewhere between $150 and $300 per year. That’s it. We're talking about $12 to $25 a month for a massive layer of financial protection.

Need more? Each additional million in coverage gets even cheaper, typically adding just $50 to $75 to your annual premium.

Of course, your final price tag isn't pulled out of a hat. Insurers look closely at your specific situation to figure out their risk.

Factors That Influence Your Premium

Every policy premium is a reflection of risk. The more likely you are to face a major lawsuit, the more you'll pay. It's that simple.

Your rate is built from a handful of key variables:

- Where you live and your personal credit history.

- The number of homes and vehicles you own.

- "Attractive nuisances" on your property, like a swimming pool, a trampoline, or even certain breeds of dogs.

- High-risk drivers in your household, especially teenagers.

Your underlying policy limits also matter. Before an insurer will sell you an umbrella policy, they need to see that you already have a solid foundation of liability coverage on your auto and home insurance. For a deeper dive into how those base costs are set, check out our guide on the average cost of homeowners insurance.

The table below breaks down the common factors that can nudge your premium up or down.

Common Factors Influencing Umbrella Insurance Premiums

| Risk Factor | Potential Impact on Premium | Reasoning |

|---|---|---|

| Number of Cars & Drivers | Higher | More vehicles and drivers, especially young ones, increase the statistical odds of a serious auto accident. |

| Number of Properties | Higher | Each additional property (like a rental home) represents another location where a liability incident could occur. |

| High-Risk Home Features | Higher | Swimming pools, trampolines, and hot tubs are common sources of guest injuries and lawsuits. |

| Certain Dog Breeds | Higher | Insurers may view breeds with a reputation for aggression as a higher risk for dog bite claims. |

| Personal Activities & Hobbies | Higher | Owning boats, RVs, or ATVs adds new avenues for potential liability claims. |

| Driving Record | Higher | A history of accidents or traffic violations signals a higher-risk driving profile. |

| Location | Varies | Premiums can be higher in more litigious states or areas with higher costs of living and larger court settlements. |

Ultimately, insurers are trying to paint a complete picture of your potential liability. The more complex your assets and lifestyle, the more they will adjust the premium to match.

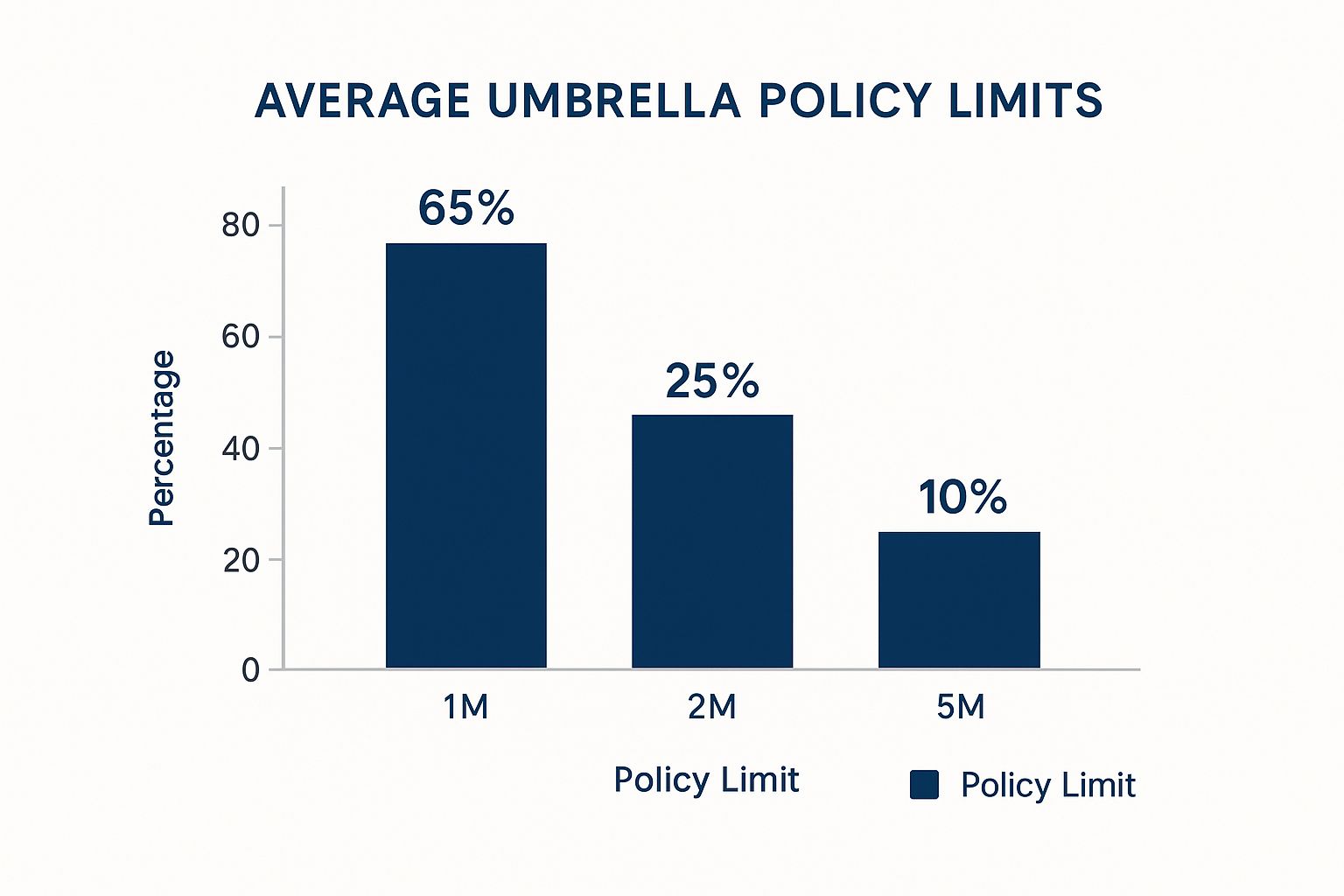

The image below gives you a clear look at where most people start.

As you can see, the $1 million policy is the go-to starting point for a reason. It provides a huge amount of protection for a very reasonable cost, making it an accessible and powerful tool for most families.

Who Really Needs an Umbrella Policy?

While just about anyone can benefit from an umbrella policy, it quickly shifts from a "nice-to-have" to a "must-have" for certain people. The question to ask yourself is simple: could a major lawsuit wipe out more than what your current auto or home insurance would pay?

If the answer is yes, it's time to look seriously at this coverage. Think of it this way: the more you have to lose, the more you need to protect it. People with significant savings, investments, or even just substantial home equity are prime candidates. An umbrella policy acts as a financial firewall, preserving the wealth you've worked hard to build when a lawsuit targets those assets.

High-Risk Profiles That Scream "Get an Umbrella Policy"

It’s not just about what you own; it's also about what you do. Certain lifestyles and responsibilities automatically crank up your risk of being sued. If you find yourself in any of these common scenarios, your need for an umbrella policy is way higher than average.

You should strongly consider this extra layer of protection if you:

- Own a home or multiple properties: Every property you own is another place where an accident can happen.

- Have teenage drivers: Let's be honest, young drivers are statistically more likely to be in a serious accident, creating a huge liability risk for the whole family.

- Frequently host parties or gatherings: The more guests on your property, the more chances for a slip-and-fall or other injury that could lead to a claim.

- Own a swimming pool, trampoline, or boat: These are what insurers call "attractive nuisances" for a reason. They significantly raise the risk of a major liability lawsuit.

- Are a landlord: Renting property to others comes with its own unique set of legal and liability headaches.

- Serve on a non-profit board: You might be surprised to learn that volunteers can sometimes be held personally liable for a non-profit's actions.

The Bottom Line: An umbrella policy isn't just for the super-rich. It's for anyone whose daily life or assets put them at a higher-than-average risk of facing a lawsuit that could financially ruin them.

How to Choose the Right Umbrella Policy

Finding the right umbrella policy isn't complicated once you know the steps. The real goal is simple: get enough coverage to fully protect your assets without buying more than you need.

So, where do you start? Begin by tallying up your total net worth. This includes all your savings, investments, home equity, and even your potential future earnings.

This number is your anchor point for figuring out how much coverage makes sense. A solid rule of thumb is to secure an umbrella policy that covers your entire net worth.

Once you have your number, the next step is to look at the insurance you already have.

Meeting the Minimum Requirements

Before an insurance company will sell you an umbrella policy, they'll want to see that you already have a decent amount of liability coverage on your existing home and auto policies.

Typically, they require underlying limits of $250,000 to $500,000. Think of it as the foundation—your umbrella policy can't be built on shaky ground.

Pro Tip: Your current insurance company is often the easiest place to begin your search. Bundling your home, auto, and umbrella policies can unlock some serious multi-policy discounts and makes managing payments and claims much simpler.

Even if you plan to bundle, it’s always a good idea to get quotes from a couple of different carriers to make sure you're getting a fair price.

Finally, read the policy documents before you sign. Pay close attention to the exclusions and understand their claims process. This final check ensures that what you think your policy covers is what it actually covers when you need it most.

A Few Final Questions on Umbrella Insurance

Let's clear up a few common questions that pop up when people are trying to wrap their heads around how umbrella policies really work.

Does It Cover My Own Injuries or Property?

That's a common point of confusion, but the answer is a firm no. An umbrella policy is purely about liability—it protects your assets when you're found responsible for someone else's injuries or property damage.

It won’t pay your own medical bills after an accident or fix your own car. That's what your health, auto, and homeowners insurance are for. Think of the umbrella as a shield for your savings, not a fund for your own recovery.

Can I Buy an Umbrella Policy from a Different Company?

Technically, you might be able to, but it's rarely a good idea and most insurers won't even allow it. They almost always require you to have your primary auto and homeowners policies with them first.

Why? Because the umbrella policy is designed to sit directly on top of those existing coverages. Keeping everything with one company makes the claims process smoother and often unlocks bundling discounts, so it’s usually the smarter move anyway.

What Is a Self-Insured Retention?

Think of a Self-Insured Retention (SIR) as a type of deductible, but it only kicks in for specific situations. It’s an amount you pay out-of-pocket before your umbrella coverage activates for a claim.

However, you typically only face an SIR for claims that are covered by your umbrella policy but not by your underlying insurance. A classic example is being sued for libel or slander. For a straightforward car accident where you max out your auto liability, there's usually no SIR—the umbrella policy just takes over where the first policy left off.

Ready to see if an umbrella policy is the right fit for your financial picture? The team at MyEasyRate Insurance can walk you through the options and find the right level of protection. Get your free quote today at https://myeasyrate.com.