Yes, if you register a vehicle in Florida, car insurance isn't optional—it's mandatory. The state law is straightforward: any vehicle with at least four wheels needs to have continuous coverage to be driven legally on Florida roads.

Florida Law Requires Car Insurance

Driving in the Sunshine State is about more than just scenic highways; it's also about meeting your legal responsibilities. Florida has what's called a "no-fault" insurance system, which is a bit different from how many other states handle things.

Essentially, it means your own insurance policy is your first line of defense for covering your own injuries after an accident, no matter who was at fault. This whole system is designed to get medical bills paid quickly and keep smaller injury claims from bogging down the court system.

To make this system work, every driver is required to carry two specific types of minimum coverage: Personal Injury Protection (PIP) and Property Damage Liability (PDL).

Understanding the Minimum Requirements

Think of these minimums as the absolute baseline you need to legally get behind the wheel in Florida. They’re the foundation of your financial responsibility as a driver.

- Personal Injury Protection (PIP): This is the heart of the no-fault law. It’s designed to cover 80% of your initial medical expenses and a slice of your lost wages after a crash, up to your policy limit. The key here is that it pays out regardless of who caused the accident.

- Property Damage Liability (PDL): This coverage kicks in to pay for the damage you cause to someone else's property. So, if you rear-end another car or accidentally back into a neighbor's fence, your PDL coverage is what pays for their repairs.

The whole point of these mandatory coverages is to ensure every driver has a basic financial backstop. It helps manage the immediate aftermath of an accident without waiting for a lengthy legal battle to decide who was to blame.

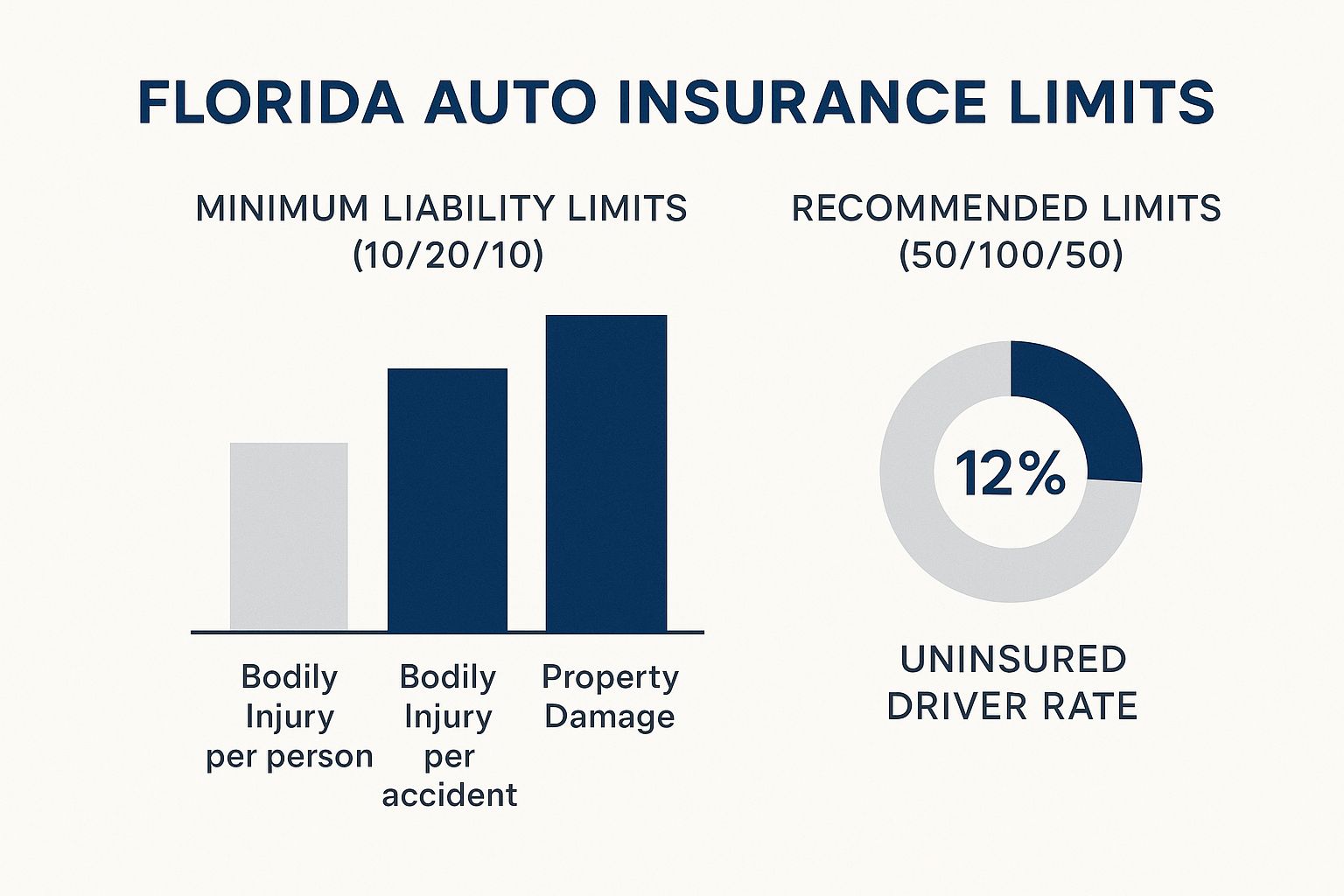

In short, Florida legally requires every driver to carry at least $10,000 in personal injury protection (PIP) and $10,000 in property damage liability (PDL). This requirement is the cornerstone of the state's no-fault system, which helps ensure injured parties can get immediate medical benefits. For a deeper dive into the issues facing Florida's drivers, the Florida Justice Association offers some valuable insights.

To keep it simple, here’s a quick summary of exactly what the state demands for every registered vehicle.

Florida's Mandatory Car Insurance Requirements at a Glance

This table breaks down the two types of coverage and the minimum amounts you absolutely must have to drive legally in Florida.

| Coverage Type | Minimum Required Amount | What It Covers |

|---|---|---|

| Personal Injury Protection (PIP) | $10,000 | Your own medical bills and lost wages after an accident, regardless of who is at fault. |

| Property Damage Liability (PDL) | $10,000 | Damage you cause to another person's vehicle or property in an accident where you are at fault. |

While these are the legal minimums, many drivers find this level of coverage is not nearly enough to handle the costs of a serious accident. We'll explore why you might want more than the bare minimum a bit later.

Navigating Florida’s No-Fault Insurance Law

Florida is a "no-fault" state when it comes to car insurance, a term that trips up a lot of drivers. The easiest way to think about it is this: after an accident, your own insurance policy is your first line of defense for your own injuries, no matter who was at fault.

This system was designed to get money into injured people's hands fast. Instead of getting stuck in a long, drawn-out investigation to figure out who caused the crash, you turn to your own policy first to get your initial medical bills paid.

Breaking Down Personal Injury Protection (PIP)

The engine of Florida’s no-fault law is Personal Injury Protection, which everyone just calls PIP. This is the specific coverage that handles your medical bills and lost pay after a wreck. Because insurance is mandatory here, every single driver is required to carry this protection.

Think of your PIP coverage as a small, dedicated fund you can tap into immediately after an accident. It’s built to provide quick financial relief, letting you focus on getting better instead of worrying about how you're going to pay for that first emergency room visit.

Under Florida law, your PIP coverage must pay for 80% of your initial medical bills and 60% of your lost wages, up to a total limit of $10,000. This rule applies whether you caused the crash or were the innocent victim.

And this coverage isn't just for you. It's designed to help a few other people, too:

- Your passengers: If they get hurt while riding in your car, your PIP can help with their initial medical costs.

- Family in your household: Relatives living with you are often covered by your PIP if they're injured in someone else's car.

- Pedestrians or cyclists: If you're involved in a crash that injures a pedestrian or someone on a bike, your PIP coverage can extend to them.

The whole point is to make sure immediate medical needs get addressed right away, which is the core mission of the no-fault system.

Understanding Property Damage Liability (PDL)

While PIP handles the people, Property Damage Liability (PDL) handles the stuff. This is the second piece of mandatory coverage in Florida, and it pays for the physical damage you cause to someone else's property.

It's critical to understand that PDL does not cover your own car. It only pays for the things you break.

Think of PDL as the coverage that protects your wallet when you’re on the hook for damaging someone else's property in a crash. It's a key reason why car insurance is mandatory in Florida—it ensures you have a way to pay for the mess you made.

This coverage kicks in for common accident scenarios, like:

- Damage to another car: If you cause a collision, your PDL is what pays to fix the other person's vehicle.

- Damage to property: If you swerve and take out a mailbox, a fence, or even scrape the side of a building, your PDL is there to cover those repair bills.

The state minimum for PDL is $10,000. But you can probably imagine how quickly the repair bill for a new SUV or a damaged storefront can blow past that number. Carrying only the state minimum can be a huge financial gamble.

A Real-World Accident Scenario

Let’s walk through a simple crash to see how these two coverages work together. Say you're not paying attention and you rear-end someone at a stoplight. Both you and the other driver have some minor injuries, and their car's bumper is smashed.

Here’s how your mandatory Florida insurance would respond:

- Your Injuries: You’d file a claim with your own insurance company. Your $10,000 in PIP would pay 80% of your medical bills and 60% of any lost wages.

- The Other Driver's Injuries: This is the "no-fault" part. The other driver also turns to their own PIP policy first to cover their initial medical costs, even though you were the one who caused the accident.

- The Other Car's Damage: Because you were at fault for the property damage, your $10,000 in PDL coverage would pay to repair the other person's car.

This example really shows the no-fault system in action. Instead of one insurance company handling everything, each driver's policy takes care of their own initial injuries, while the at-fault driver's liability coverage pays for the property damage.

Why Minimum Coverage Is Not Enough

Meeting Florida's legal car insurance requirements is one thing. Being genuinely protected from a financial nightmare is something else entirely. While carrying $10,000 in PIP and $10,000 in PDL makes you legal on paper, it leaves a huge, dangerous gap between what the law says you need and what a real-world accident actually costs.

Think of the state minimums as a leaky life raft. Sure, it might keep you afloat if you fall into a calm pond, but it’s the last thing you want when a real storm hits. A single, seemingly minor accident can rack up costs that completely dwarf these minimums, leaving you on the hook for thousands—or even hundreds of thousands—of dollars out of your own pocket.

The Real Cost of a Modern Accident

Let's put that $10,000 PDL limit into perspective. Imagine you cause a fender-bender with a newer SUV. With all the sensors, cameras, and specialized parts in modern vehicles, the average cost for repairs has skyrocketed. Even minor cosmetic damage can easily top $5,000. If you hit a luxury car or a brand-new truck, that $10,000 limit can disappear almost instantly.

So, what happens then? If the total repair bill is $18,000, your insurance pays the first $10,000. You are personally responsible for the remaining $8,000. That’s a massive out-of-pocket hit that the bare-bones mandatory coverage in Florida simply doesn't prepare you for.

This image really drives home just how different the minimum requirements are from more realistic, recommended coverage.

The visual shows the massive gap in protection, highlighting how much financial risk drivers are taking on just to meet the bare minimum.

Bodily Injury Liability: The Missing Piece

The single biggest hole in Florida’s mandatory insurance law is that it doesn't require Bodily Injury Liability (BIL) coverage. While your PIP helps with your own initial medical bills, BIL is what pays for the injuries you cause to other people when you're at fault.

If you cause a crash that seriously injures another driver or their passengers, their medical bills can climb into the tens or hundreds of thousands of dollars in a flash. Without BIL coverage, you are personally liable for every single penny.

This could lead to your wages being garnished, liens being placed on your property, and complete financial ruin. Bodily Injury Liability isn't just another policy add-on; it's the single most important coverage for protecting your personal assets from a lawsuit.

Adding BIL is what shifts your protection from simply being "legal" to being financially secure. It’s the firewall between an unfortunate accident and a life-altering financial crisis.

The table below breaks down how a minimum policy stacks up against a more robust, recommended policy in a common accident scenario.

Comparing Minimum vs Recommended Coverage in Florida

| Scenario | Coverage with Minimum Policy ($10k PIP/$10k PDL) | Coverage with Recommended Policy (Higher Limits + BIL & UM) |

|---|---|---|

| You cause a multi-car accident. The other driver has $40,000 in medical bills, and their car has $25,000 in damage. | Your PIP covers $10,000 of your own injuries. Your PDL pays $10,000 for their car. You are personally sued for the remaining $15,000 in car damage and the $40,000 in medical bills. Total out-of-pocket risk: $55,000. | Your higher PIP provides better personal coverage. Your BIL covers the other driver's $40,000 medical bills. Your higher PDL covers the full $25,000 car damage. You walk away with no out-of-pocket costs for their damages. |

| An uninsured driver runs a red light and hits you, causing $30,000 in medical bills for you and totaling your car. | Your PIP covers $10,000 of your medical bills. You're on the hook for the remaining $20,000. You have to sue the at-fault driver (who has no insurance or assets) to recover anything for your injuries or car. | Your PIP covers initial medical bills. Your Uninsured Motorist (UM) coverage pays for the remaining $20,000 in medical costs. Your Collision coverage (part of a full coverage policy) pays to repair or replace your car. You're made whole. |

As you can see, the difference isn't just about numbers—it's about financial survival after a bad day on the road.

Protecting Yourself From Other Drivers

So what happens when you’re the victim? Unfortunately, Florida has one of the highest rates of uninsured drivers in the entire country. Simply hoping the other driver has good—or even any—insurance is a huge gamble.

This is where Uninsured/Underinsured Motorist (UM/UIM) coverage becomes absolutely essential.

- Uninsured Motorist (UM): This is your hero. It steps in to pay for your medical bills and related costs if you're injured by a driver who has no insurance at all.

- Underinsured Motorist (UIM): This protects you when the at-fault driver does have insurance, but their policy limits are too low to cover all of your medical bills.

Think of UM/UIM as a safety net that you control. It guarantees you have a way to recover when the person who hit you can't pay. With so many drivers ignoring the law, UM coverage is your personal shield against their irresponsibility. It protects your family, your health, and your financial future from someone else's mistake.

While these extra coverages do increase your premium, it's often possible to find ways to make them affordable. For anyone looking to add this critical protection, exploring tips on how to lower car insurance costs can help you get a policy that truly safeguards your assets without breaking the bank.

The Real Cost of Driving Uninsured in Florida

While car insurance is a legal must-have in Florida, plenty of drivers still roll the dice and hit the road without it. This is way more than a simple traffic ticket—it’s a massive financial gamble that can completely unravel your life after just one bad day.

The state takes this very seriously, and the penalties are designed to be a painful lesson. If you're caught driving without the required PIP and PDL coverage, the consequences are immediate, costly, and they get worse with each offense. This isn't just about fines; it's about losing your legal right to drive.

The bottom line is simple: the cost of a basic policy is always, always cheaper than the cost of getting caught.

Immediate Penalties for a First Offense

The moment a police officer cites you for driving without insurance, the Florida Department of Highway Safety and Motor Vehicles (FLHSMV) gets involved. For a first offense, you’re looking at an immediate suspension of both your driver's license and vehicle registration.

You can’t legally drive any vehicle until you fix the problem. To get your driving privileges back, you have to:

- Show proof of a valid Florida insurance policy.

- Pay a $150 reinstatement fee.

And that’s just for the first time. The costs and headaches pile up fast if it happens again.

Escalating Consequences for Repeat Offenses

Florida law comes down even harder on repeat offenders. If you get caught without insurance a second time within three years, the penalties get much steeper. The reinstatement fee jumps to $250.

A third offense within that same three-year window? Now you're paying a $500 reinstatement fee. At this point, the state will likely force you to file an SR-22 form. This is a special certificate your insurance company files to prove you have coverage.

An SR-22 essentially labels you as a high-risk driver to the state. That tag almost guarantees you’ll be paying much, much higher insurance premiums for several years. It's a costly and long-lasting consequence of breaking the rules.

Despite these tough penalties, Florida has a shocking number of uninsured drivers. In 2023, estimates suggest around 20% of Florida's 16.4 million licensed drivers are on the road without coverage, putting us at the 6th highest rate in the country. This is a huge reason why carrying your own solid coverage is so critical.

The Financial Devastation of an At-Fault Accident

The state-imposed fees are pocket change compared to the financial ruin you’ll face if you cause an accident while uninsured. Without liability coverage, you are personally on the hook for every single dollar of damage and every medical bill you cause.

Let’s play this out. Imagine you cause a moderate crash that results in $15,000 in damage to the other car and $20,000 in their medical bills. Without insurance, you owe that entire $35,000 out of your own pocket. The other driver can—and will—sue you personally to get it back.

This legal judgment can lead to:

- Wage Garnishment: A court can order your employer to take money directly out of your paycheck and send it to the person you owe.

- Property Liens: A lien can be placed on your home or other property, which means you can’t sell it until the debt is paid.

- Asset Seizure: In the worst-case scenario, your personal property can be seized and sold to cover what you owe.

This isn’t just about dealing with the aftermath of a crash; it’s about being thrown into a long-term legal and financial nightmare. For insured drivers, knowing how to file a car insurance claim is the first step to recovery—a process that highlights just how vital that coverage is. At the end of the day, the price of a basic insurance policy is a tiny fraction of the potential debt from a single uninsured accident.

Understanding Florida’s High Insurance Premiums

If you live in Florida and feel like your car insurance bill is out of control, you're not wrong. The Sunshine State consistently ranks as one of the most expensive places in the entire country to insure a vehicle.

This isn't just one single problem. It’s more like a "perfect storm" of factors that all converge here, driving up costs for pretty much everyone. Understanding what’s happening behind the scenes—from wild weather to crowded highways and a messy legal system—is the first step to figuring out why your premium is what it is.

The Impact of Severe Weather

Florida's beautiful, sunny coastline is also a magnet for hurricanes and tropical storms. When these massive weather events hit, they cause widespread vehicle damage, triggering a flood of claims all at once. Cars get totaled by floodwaters, crushed by falling trees, and battered by flying debris.

This constant, recurring risk means insurance companies have to charge more upfront to build up cash reserves for the next inevitable disaster. The numbers are staggering. Since 1980, nearly 23% of all U.S. billion-dollar weather disasters have hit Florida. After Hurricane Ian alone, insurers had to deal with claims for over 100,000 destroyed vehicles.

It’s gotten so bad that for every $1.00 insurers collect in premiums, they are paying out $1.12 in claims and expenses. You just can't sustain a business like that without raising rates.

High Population Density and Heavy Traffic

Florida is the third most populous state in the nation, and a huge chunk of that population is squeezed into dense urban areas like Miami, Tampa, and Orlando. Put simply, more cars packed onto the same roads means more accidents. It's a direct cause-and-effect.

Add millions of tourists who are unfamiliar with the local roads to the mix, and you have a recipe for a high frequency of collisions. More crashes lead to more claims for both property damage and injuries, which forces insurers to raise the base rates for everyone in the region.

A higher volume of claims is a foundational reason for higher premiums. Insurers calculate risk based on historical data, and in Florida, the data points to a consistently high likelihood of accidents occurring in its congested metropolitan corridors.

A Litigious Culture and Insurance Fraud

Another huge piece of the puzzle is Florida's reputation for being a very lawsuit-happy state, especially when it comes to car accidents. For years, the state's no-fault PIP system was a prime target for fraudulent medical clinics and dishonest attorneys who would inflate injury claims or file massive lawsuits over minor fender-benders.

This created enormous costs for insurance companies, who had to spend a fortune on legal fees fighting suspicious claims and paying out inflated settlements. Of course, those costs didn't just disappear—they were passed directly to you, the policyholder, in the form of higher premiums.

Recent legal reforms are trying to fix this, but the legacy of that system is still a major reason your rates are so high. If you're tired of paying for it, your best defense is to shop around. A great place to start is our guide on how to compare car insurance rates in Florida to find a more affordable policy.

Common Questions About Florida Car Insurance

Florida's insurance rules can feel a little tricky, especially when life throws you a curveball. Even when you know the basics, real-world situations can leave you wondering if you're still compliant. Let’s clear up a few of the most common questions we hear from drivers every day.

We'll tackle what happens if your coverage slips, how to handle a car that's just sitting in the garage, and the first steps you need to take as a new resident.

What Happens If My Insurance Lapses for Just One Day?

This is a big one. In Florida, there is no grace period for mandatory car insurance. Zero. The state’s system is electronic and automated, and your insurance company is required by law to instantly notify the Florida Highway Safety and Motor Vehicles (FLHSMV) the moment your policy is canceled or lapses.

Even a single day without coverage can trigger that notification. Once the state gets the alert, it sends a notice demanding proof of new insurance. If you don't provide it right away, the consequences are exactly the same as if you were pulled over without a policy.

The state can suspend your driver's license, vehicle registration, and license plate. To get everything reinstated, you'll have to show proof of new, active coverage and pay a reinstatement fee, which starts at a painful $150 for the first offense.

Because this system is automated, there's virtually no wiggle room. Keeping your coverage continuous isn't just a good idea—it's a hard-and-fast rule with swift penalties.

Do I Need Insurance on a Car I Don’t Drive?

This trips a lot of people up. The simple rule in Florida is this: if a car has a valid license plate and registration, it must be insured. It doesn't matter if it's parked in your garage, sitting in the driveway, or stored somewhere else. As long as it's registered, it has to meet the state's minimum PIP and PDL requirements.

Letting the insurance lapse on that registered-but-parked car will trigger the same exact penalties—a suspended license and registration.

So, what if you have a car you truly won't be driving for a long time, like a project car or one you're storing for the season? The only way to legally drop the insurance is to first surrender your license plate and registration at a Florida driver license or tax collector's office. Once you've turned in the plate, the car is no longer officially registered for road use, and the mandatory insurance rule no longer applies.

I’m Moving to Florida—What Do I Need to Do?

Welcome to the Sunshine State! Once you're here and have established residency, the clock starts ticking. Florida gives you just 30 days to get a Florida driver's license.

Before you can register your vehicle, however, you must have a Florida-compliant auto policy in place. You absolutely cannot register your car here using your old out-of-state insurance.

Here are the key steps to follow, in order:

- Buy Florida Insurance: First things first. Call an agent and purchase a policy that meets Florida’s minimum $10,000 PIP and $10,000 PDL coverage.

- Get Your Florida Driver's License: Head to a local service center to swap your out-of-state license for a Florida one.

- Register Your Vehicle: With your new Florida license and proof of Florida insurance in hand, you can finally register your vehicle and get your new plates.

Don't drag your feet on this. Failing to switch everything over in a timely manner can create a real headache, so it's best to knock it out as soon as you settle in.

Navigating these rules is always easier with an expert in your corner. At MyEasyRate Insurance, we specialize in helping Florida drivers find the perfect coverage for their needs, ensuring you're always protected and compliant. Get your free, no-obligation quote today at https://myeasyrate.com.