Rental property insurance is a specific type of policy built to protect landlords from the financial fallout that can come with owning a rental. It's not the same as a standard homeowner's policy. Instead, it’s designed to cover the unique risks that pop up when you have tenants, like liability claims or lost rent, on top of protecting the actual building.

If you rent out property, this insurance isn't just a good idea—it's essential.

Why Your Rental Needs Specialized Insurance Coverage

It's easy to think of your rental property as just another house, but that’s a mistake. You have to see it as a business. And like any business, it comes with its own set of risks that demand specialized protection. A regular homeowner's policy is designed for a home you live in, not one you rent out, and it’s just not built to handle the liabilities that come with tenants.

Think of it like owning a restaurant. You wouldn’t rely on your personal home insurance to cover a customer who slips and falls, or a kitchen fire that shuts down your business. The risks are completely different. Your rental property is the same—it’s an income-generating business that exposes you to financial threats only true rental property insurance coverage can handle.

The Homeowner's Policy Gap

A standard homeowner's policy has a major blind spot: it usually excludes or severely limits coverage for any business activities happening on the property. Since renting out your home is a business, any claim related to your tenants could be flat-out denied. For example, if a tenant's guest gets hurt on your property and decides to sue, your homeowner's insurance will almost certainly refuse to cover the legal bills or any settlement. That leaves you and your personal assets dangerously exposed.

And that's not the only gap. A standard policy misses one of the biggest financial risks a landlord can face.

Loss of Rental Income coverage is a game-changer. If a covered disaster, like a fire or major storm damage, makes your property unlivable during repairs, this coverage replaces the rent you would have collected. It keeps your cash flow going when you need it most.

Protection Tailored for Landlords

Landlord insurance is built from the ground up to shield you from the realities of being a landlord. It’s about more than just protecting the bricks and mortar; it’s about protecting your financial stability as a property owner. This specialized policy understands that someone else is living in your asset, which introduces a whole new world of potential problems.

The core protections designed specifically for landlords include:

- Property Damage Protection: This covers the physical structure of your rental—the house itself—from perils like fire, windstorms, and certain kinds of water damage.

- Liability Coverage: This is your financial backstop if a tenant or their guest is injured on the property and you're found legally responsible. It helps pay for their medical bills and your legal defense.

- Loss of Income: As mentioned, this is the crucial coverage that keeps the rent money coming in if your property is temporarily uninhabitable after a covered event.

It's also critical to remember what your policy doesn't cover: your tenant's personal belongings. That’s their responsibility. Many savvy landlords even require their tenants to get their own protection. You can learn more by checking out our guide on why renters insurance matters for protecting belongings. Getting this distinction right is fundamental to properly managing your property's risk.

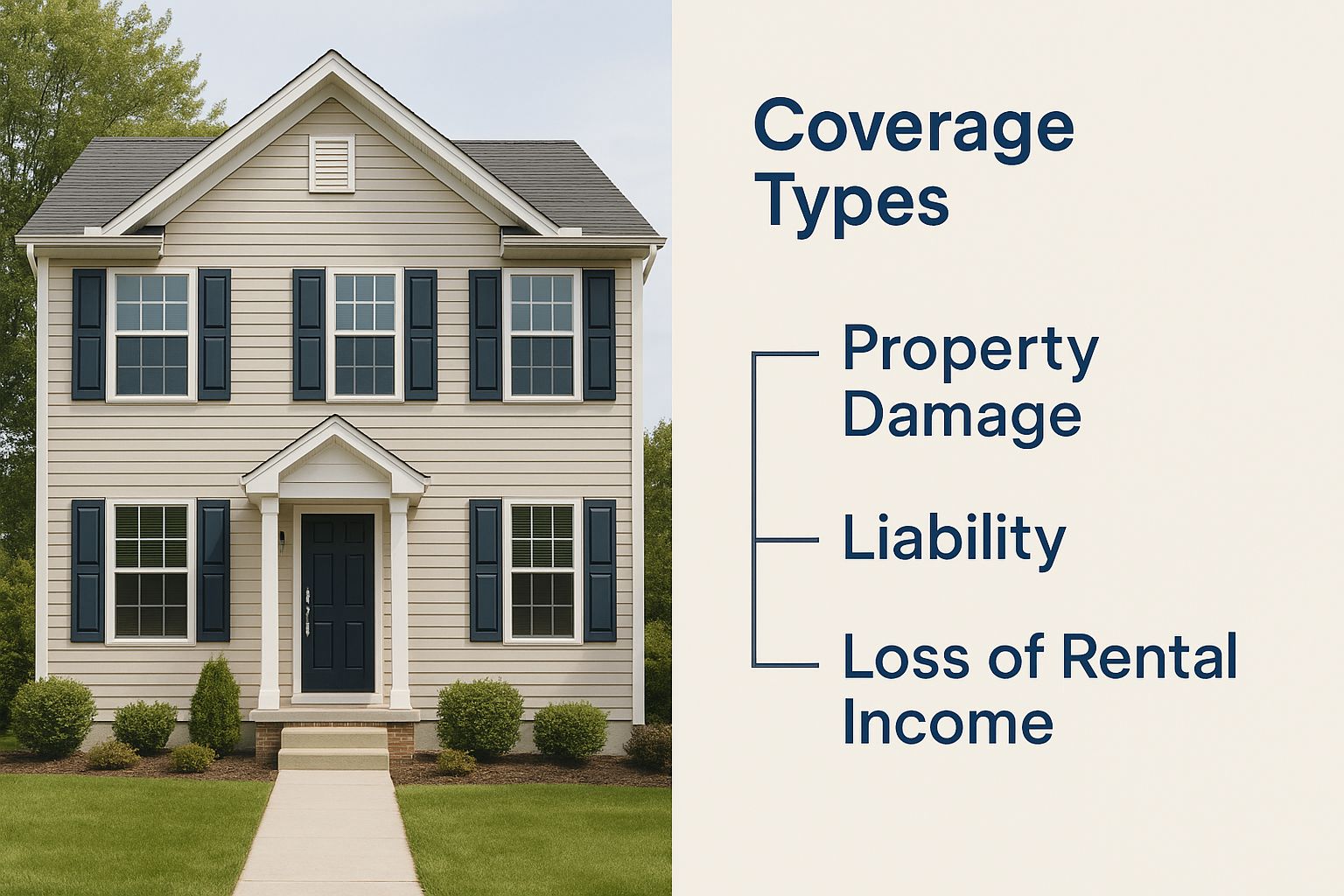

Decoding Your Core Landlord Insurance Policy

Think of your landlord insurance policy as a custom-built financial toolkit. Each tool inside is designed to fix a very specific type of problem. Just buying the toolkit isn't enough; you need to know what each piece does so you're ready when something goes wrong. Let's open it up and look at the three essential tools that form the foundation of any solid rental property insurance plan.

This is the bedrock of your protection, covering the big, expensive stuff.

As you can see, each coverage type tackles a unique risk, protecting everything from the physical building to your bottom line.

Dwelling Coverage: The Protector of Your Physical Asset

This is the big one. Dwelling coverage is all about protecting the physical structure of your rental property—the actual building. We're talking about the roof, walls, foundation, and even the built-in systems like plumbing and electrical. It’s what pays to rebuild or repair your asset when it gets damaged.

Imagine a nasty hailstorm rolls through and shreds the siding on one side of the house. Dwelling coverage is what you’ll use to pay the contractor to make those repairs, restoring your property to the condition it was in before the storm.

This protection isn't just for the main house, either. It almost always extends to other structures on the property, like:

- Detached Garages: If a fire starts in the separate garage, this coverage helps rebuild it.

- Fences: A windstorm blows over a section of the backyard fence? Your policy can help pay for the replacement.

- Sheds: That little storage shed out back is usually covered, too.

Just remember, this part of the policy is for your property only. It does not cover any of your tenant's personal belongings.

Liability Protection: Your Shield Against Lawsuits

Liability protection might just be the most important part of your entire policy. It's your financial bodyguard, stepping in if you're found legally responsible for an accident that injures a tenant or a visitor on your property.

Here's a classic example: a wobbly handrail on the porch that you've been meaning to fix finally gives way while a tenant is carrying in groceries. They fall, break an ankle, and sue you for their medical bills and lost wages.

This is exactly what liability coverage is for. It helps pay for the injured person's medical expenses, your legal defense fees, and any court-ordered settlement, all the way up to your policy limit. Without it, a single slip-and-fall accident could put your personal savings, and even your home, at risk.

Given how expensive lawsuits are, strong liability protection is non-negotiable for any serious landlord.

Loss of Rental Income: Your Cash Flow Lifeline

Okay, so a kitchen fire makes your property unlivable. Your tenants have to move out for three months while repairs are underway. The problem? You still have a mortgage payment, property taxes, and insurance premiums due every month, but zero rent coming in. This is where Loss of Rental Income coverage saves the day.

Sometimes called Fair Rental Value, this coverage replaces the rent you would have collected while the property is being repaired after a covered claim. It’s a business-saver, plain and simple. It keeps your cash flow from screeching to a halt and prevents a temporary setback from snowballing into a full-blown financial crisis.

To make it even clearer, let's break down these core coverages into a simple table.

Standard Landlord Insurance Policy Breakdown

This chart sums up the main components of a typical policy, showing what each one protects and how it works in the real world.

| Coverage Component | What It Protects | Example Scenario |

|---|---|---|

| Dwelling Coverage | The physical structure of your rental property and attached structures. | A tree falls on the roof during a storm, requiring major repairs to the rafters and shingles. |

| Liability Protection | Your personal assets against lawsuits from injuries on your property. | A visitor trips on a cracked sidewalk, sues for their medical bills, and you are found liable. |

| Loss of Rental Income | Your rental income stream if the property becomes uninhabitable due to a covered loss. | A pipe bursts, causing extensive water damage that requires your tenants to move out for two months during repairs. |

Together, these three pillars form a powerful defense for your rental business. It's no surprise that more landlords are recognizing their importance.

In fact, projections show the European landlord insurance market is expected to hit $27.77 billion by 2028, growing at an annual clip of about 7.94%. This growth reflects a clear trend: landlords are getting serious about protecting their investments. You can dive deeper into these trends in the full research on landlord insurance from Cognitive Market Research.

Strategic Policy Add-Ons for Complete Protection

A standard landlord policy is a great starting point, but every rental property comes with its own quirks and risks. It's best to think of optional coverages—or "endorsements," as they're called in the industry—as strategic investments, not just extra costs.

These add-ons are designed to plug the specific gaps in a basic policy, letting you build a truly customized shield for your business. Let's walk through some of the most valuable ones you can add to protect yourself from common landlord headaches.

Rent Guarantee Insurance

One of the biggest financial fears for any landlord is a tenant who simply stops paying rent. The eviction process can drag on for months, all while your mortgage, taxes, and maintenance bills keep coming due. That's where Rent Guarantee Insurance becomes a lifesaver.

This add-on reimburses you for lost rental income when a tenant defaults. It’s a safety net for your cash flow, giving you the financial stability to get through a lengthy eviction without draining your savings.

Demand for this protection is climbing fast. The global rent guarantee insurance market is growing at an estimated 8.7% each year, partly because new tech makes it easier and more affordable for landlords to get covered.

Vandalism Coverage

What happens if your property sits empty between tenants? A vacant home can become a magnet for trouble, from broken windows and graffiti to serious interior damage. Most standard policies won't cover this kind of malicious mischief if the property has been vacant for a while, usually 30 to 60 days.

That’s a huge gap in your protection. Vandalism Coverage is an endorsement specifically designed to pay for repairs from intentional damage while the property is unoccupied. If you expect any turnover or longer vacancies, this is a must-have. For a deeper dive, check out our guide on insurance options for a vacant home.

Building Code Upgrade Coverage

Here's a scenario that catches too many landlords by surprise. Imagine a fire damages half of your older rental unit. As you start rebuilding, the city inspector informs you that local building codes have been updated. Now, you’re legally required to upgrade the electrical and plumbing for the entire building, not just the damaged part.

A standard policy only pays to restore the property to its previous condition. Those mandatory upgrades could cost you tens of thousands out-of-pocket.

Building Code Upgrade Coverage, sometimes called Ordinance or Law Coverage, steps in to pay for these expensive, legally required updates. It ensures a major repair doesn't spiral into a financial catastrophe.

This endorsement is especially crucial if you own an older property, where the gap between original construction and modern codes can be massive.

Other Valuable Endorsements to Consider

Beyond those big three, a few other add-ons can fortify your policy depending on your property and location.

- Water Backup Coverage: Protects against damage from a backed-up sewer or drain—a messy and expensive event that is almost always excluded from standard landlord policies.

- Landlord Contents Insurance: If you furnish your rental with appliances, couches, or other items, this covers your belongings from damage or theft. It does not cover your tenant’s personal property.

- Theft Coverage: Provides protection if items you own are stolen from the property, like a lawnmower from the shed or tools from the garage.

By taking a hard look at your property’s weak spots, you can strategically pick the add-ons that deliver real value and peace of mind.

Understanding Common Policy Exclusions

Knowing what your insurance policy doesn't cover is just as important as knowing what it does. Think of your policy as a protective bubble around your investment. Exclusions are the specific things that this bubble simply can't deflect, leaving you exposed if you aren't prepared.

Understanding these built-in limitations is critical for avoiding expensive surprises. A standard rental property insurance coverage plan is robust, but it’s not designed to cover every possible scenario. Ignoring the fine print on exclusions is a classic mistake that can turn a manageable incident into a financial disaster.

Tenant Personal Property

Let’s start with the most common point of confusion: your tenant’s stuff. Your landlord policy is built to protect your property—the building, the garage, any appliances you own inside. It does not cover your tenant’s furniture, electronics, clothing, or other personal items.

If a kitchen fire guts the room, your policy helps rebuild the walls and replace your stove. But it won’t pay a dime for your tenant’s ruined dining set. This is a crucial distinction and exactly why your tenants need their own renters insurance.

By requiring tenants to carry renters insurance as a condition of the lease, you create a clear line of responsibility. This simple step protects your tenants and prevents disputes over who should pay for their losses after a covered event.

General Wear and Tear

Insurance is for sudden and accidental damage, not the slow, inevitable decline of property over time. An aging dishwasher that finally stops working or a furnace that gives out after 15 years of service are considered maintenance issues, not insurable events.

These situations fall under wear and tear, a standard exclusion in every policy. Your insurance won't pay to replace an old appliance just because it’s reached the end of its life. As the owner, budgeting for routine maintenance and eventual replacement of systems and appliances is just part of the financial plan.

High-Risk Natural Disasters

While your policy covers many common perils like fire and windstorms, it almost always excludes the big, catastrophic natural disasters. Events that typically require their own separate, specialized policies include:

- Floods: Damage from rising water—whether from overflowing rivers, storm surges, or heavy downpours—is not covered. Flood insurance is a separate policy, usually obtained through the National Flood Insurance Program (NFIP).

- Earthquakes: Shaking, ground movement, and the resulting structural damage are excluded. If your property is in a seismically active area, you’ll need to purchase a separate earthquake policy.

- Landslides and Mudflows: These earth movements are also standard exclusions and require specialized coverage.

To really nail down the division of responsibility between you and your tenant, this table makes it crystal clear.

Coverage Comparison: Landlord vs. Tenant Responsibility

| Item/Event | Covered by Landlord Insurance? | Covered by Renters Insurance? |

|---|---|---|

| Fire Damage to the Building | Yes | No |

| Tenant's Laptop Destroyed in Fire | No | Yes |

| Guest Slips and Falls on Porch | Yes (Liability) | No |

| Appliance Failure from Old Age | No | No |

| Flood Damage to the Property | No (Requires Flood Policy) | No (Requires Flood Policy) |

By understanding these exclusions up front, you can proactively seek the right additional coverage, manage your tenant's expectations, and build a much more resilient investment strategy. No surprises, no gaps.

Filing a Claim Without Losing Your Mind

When something goes wrong at your rental, that insurance policy you’ve been paying for suddenly becomes the most important document you own. Knowing how to handle the claims process is the difference between a quick, relatively painless resolution and a drawn-out nightmare. The key is to stay calm and methodical.

The first few moments after you discover the damage are critical. Your only two jobs are to make sure everyone is safe and to stop the problem from getting any worse.

Your First Moves After a Crisis

Once the immediate danger is over, it’s time to switch into documentation mode. What you do right now sets the stage for the entire claim, so being thorough is your best friend. Don't put this off.

- Become a Photographer. Grab your smartphone and document everything. Take wide shots to show the scope of the damage and get close-ups of specific problems. You can't take too many photos or videos. This visual proof is your single most powerful tool.

- Stop the Bleeding. Your policy requires you to mitigate further damage. That could mean throwing a tarp over a busted roof to keep the rain out or boarding up a shattered window. Make sure you keep every single receipt for materials you buy—these temporary fixes are almost always reimbursable.

- Make the Call. Get on the phone with your insurance agent or the company's claims hotline as soon as you can. Have your policy number ready and give them a clear, simple rundown of what happened. They’ll assign a claims adjuster to your case.

Staying organized from the jump will save you a world of headaches later on.

Think of yourself as the general contractor for your own claim. Start a folder—digital or physical—for every photo, receipt, and email. Log every phone call: who you spoke to, the date, and what was said.

Working with Your Insurance Adjuster

The adjuster is the person your insurer sends to investigate the damage, figure out what it will cost to fix, and determine how much they'll pay. The best approach is to be cooperative and professional. Give them all the documentation you’ve collected and be ready to walk them through the property.

But remember, you have to be your own advocate. If the adjuster’s estimate feels low, don't just accept it. Get your own quote from a trusted, independent contractor. If there’s a big difference, show your contractor’s estimate to the adjuster and calmly explain the discrepancies. A data-backed conversation is always more effective than an emotional one.

The insurance industry itself is huge and always changing to handle claims better. The global property and casualty insurance market is expected to grow from $3.97 trillion in 2024 to an incredible $8.81 trillion by 2034. This boom is fueled by new tech in claims processing and more property owners understanding the need for solid coverage. You can dig into these property and casualty insurance market trends to see where the industry is headed.

What to Do if Your Claim is Disputed or Denied

Getting a "no" from your insurance company isn't the end of the road. Don't panic.

Your first step is to ask for a formal denial letter. This document must explain why they denied the claim and point to the specific language in your policy they're using to justify it. Read that section of your policy yourself to see if you agree with their take.

If you’re convinced they got it wrong, you have options. You can file an official appeal with the insurance company, armed with any new evidence or estimates you have. If that doesn't work, you can file a complaint with your state's department of insurance. As a final step, you might consider hiring a public adjuster to fight on your behalf.

Frequently Asked Questions About Rental Property Insurance

Even after you've got the basics down, a few specific questions always pop up when you're zeroing in on the right landlord insurance policy. Getting straight answers is the only way to make smart financial moves and ensure your coverage will actually be there for you when you need it.

Let's dig into some of the most common questions we hear from landlords.

Actual Cash Value Vs. Replacement Cost

This is one of the biggest forks in the road you'll face when setting up your policy: choosing between Actual Cash Value (ACV) and Replacement Cost Value (RCV) for your property itself. The difference between them determines how much money you’ll actually get after a disaster.

- Actual Cash Value (ACV): This coverage pays to repair or replace your property minus depreciation. Think of it like the Kelley Blue Book value of a car. It pays for what the building was worth the moment before it was damaged, not what it costs to build it new.

- Replacement Cost Value (RCV): This is the good stuff. RCV pays the full, current cost to rebuild or repair your property with similar, new materials, without any deduction for age or wear and tear.

Sure, RCV means a higher premium. But it's the only option that gives you the real funds needed to completely rebuild after a total loss, which is a non-negotiable safety net for any serious investor.

How Much Liability Coverage Do I Really Need?

While a standard policy might start you off with $300,000 in liability coverage, that's often not enough. Most seasoned experts will tell you to carry a bare minimum of $1 million. A single serious slip-and-fall on your property can easily blow past a lower limit, leaving your personal assets exposed to a lawsuit.

The smartest play here is to get a separate umbrella liability policy. It's an surprisingly affordable way to add an extra layer of protection that only kicks in after your main landlord policy is maxed out. It’s a powerful financial backstop.

You also have to be honest about your property's specific risks. Got a swimming pool, trampoline, or even an old treehouse? These are "attractive nuisances" in insurance-speak, and they dramatically increase your risk profile, demanding higher coverage limits.

What About a Tenant's Pet? And Can I Get a Discount?

One question that comes up all the time is: "Am I covered if my tenant's dog bites someone?" The honest answer is, it depends. Some policies cover it, some specifically exclude "high-risk" breeds like pit bulls or rottweilers, and others wash their hands of animal liability completely. You must ask your agent about this directly.

Finally, can you save money by bundling your landlord and primary home insurance? Absolutely. Most carriers offer some of their best discounts for bundling multiple policies. As insurance costs climb, shopping around and bundling is one of the easiest ways to keep your premiums in check.

If you're thinking about moving your policies for a better deal, our guide on how to switch insurance companies breaks down the process step-by-step. It’ll help you make the change without creating any gaps in your critical rental property insurance.

At MyEasyRate Insurance, we live and breathe this stuff. Our agents specialize in helping landlords find the right protection for their investments. We can help you compare policies, find every last discount, and build a plan that lets you sleep at night. Protect your rental business by visiting us at https://myeasyrate.com to get a personalized quote today.