Let's be clear about one thing right away: standard homeowners insurance and vacant properties do not mix. Your regular policy isn't designed for an empty house, and if you try to file a claim after it’s been vacant for 30 to 60 days, you're almost guaranteed to be denied. This is all thanks to a "vacancy clause" that effectively shuts off coverage for major risks like vandalism or water damage. To truly protect your asset, you need a specialized vacant home policy.

Why Your Standard Home Insurance Won't Cover an Empty House

Think of your home insurance policy like a security guard who only shows up for their shift when someone is living in the house. The moment the property is truly vacant, that guard walks off the job, leaving the place wide open to all sorts of trouble. It's a massive—and costly—misunderstanding to assume your normal policy will protect an empty building.

The reason for this lies in a small but powerful part of your policy called the vacancy clause. This clause kicks in after the property has been empty for a specific period, usually 30 to 60 consecutive days. Once it’s triggered, your coverage for some of the biggest threats to an empty home can be severely limited or even completely erased.

The Critical Difference: Unoccupied vs. Vacant

Insurers see two very different scenarios, and knowing the distinction is key to keeping your coverage intact.

- Unoccupied: This is when the home is still furnished and ready to be lived in, but the residents are just temporarily away—maybe on a long vacation or a work assignment. The key is, they intend to return.

- Vacant: This is a whole different ballgame. A vacant home is empty of both people and their stuff. It doesn't have the basic furniture and personal items needed for someone to live there, signaling that no one is coming back anytime soon.

While a standard policy can usually handle a home being unoccupied for a while, it views a vacant property as a huge red flag. Without someone around, a tiny pipe leak can turn into a full-blown flood, causing catastrophic damage before anyone notices. An empty house is also a magnet for vandals, thieves stealing copper pipes, and even squatters.

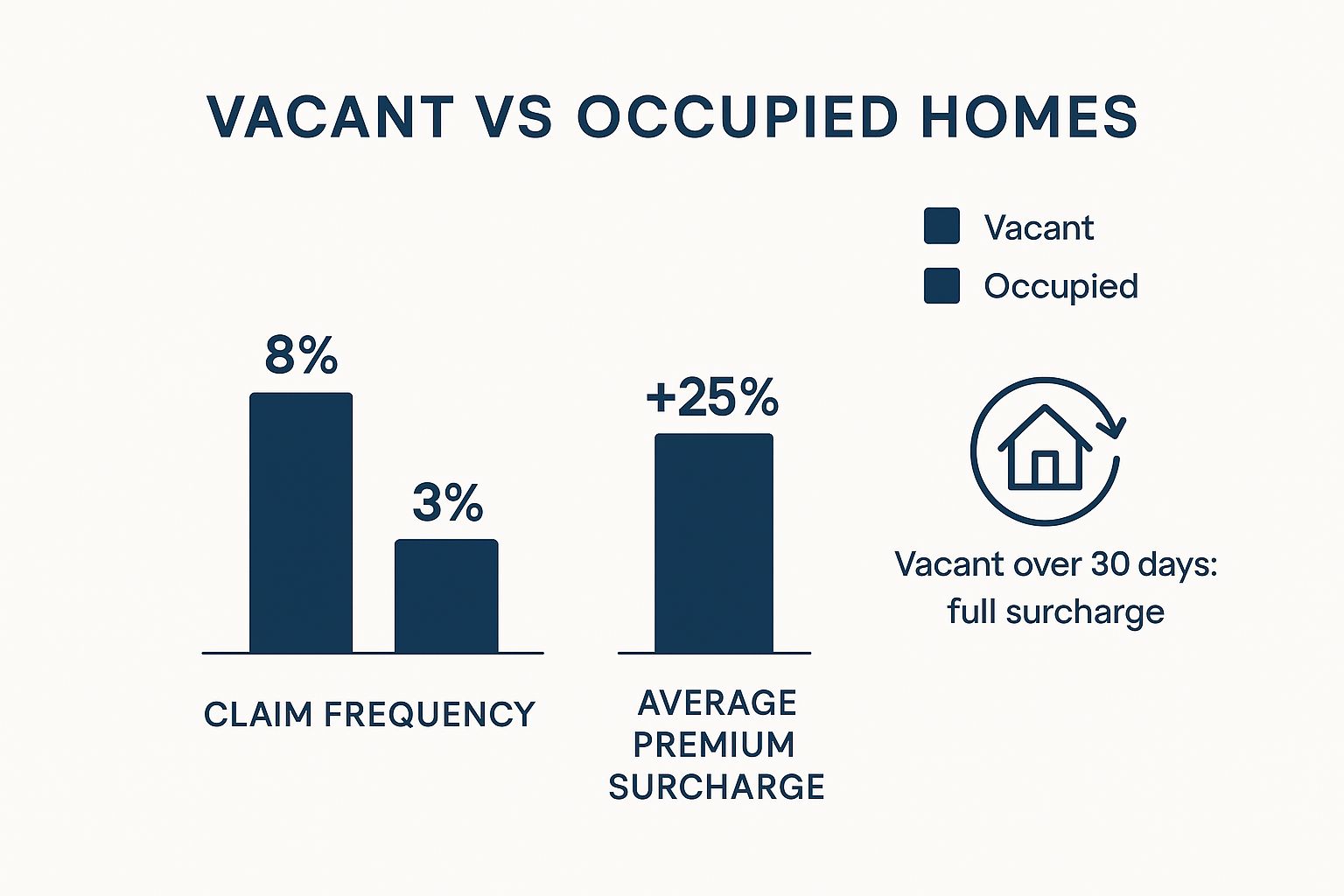

The numbers tell a sobering story about the difference in risk and cost between vacant and occupied homes.

As you can see, the increased risk isn't just theoretical—it leads directly to higher costs and more frequent claims.

To put the coverage differences in black and white, here’s a quick comparison of how a standard policy handles a vacant property versus a specialized vacant home policy.

Standard Homeowners Policy vs Vacant Home Insurance Coverage

| Risk/Peril | Standard Policy Coverage (When Vacant) | Vacant Home Insurance Coverage |

|---|---|---|

| Vandalism | Typically Excluded after 30-60 days | Usually Included (often a core feature) |

| Water Damage (e.g., burst pipe) | Often Excluded or severely limited | Generally Covered, may require winterization |

| Fire & Lightning | Coverage may remain but can be reduced | Fully Covered as a named peril |

| Theft | Almost always Excluded | Typically Excluded for contents, but covers building theft (e.g., fixtures) |

| Liability (e.g., trespasser injury) | Coverage might continue but can be challenged | Included, providing essential protection |

This table makes it crystal clear: relying on a standard policy for a vacant home leaves you dangerously exposed to some of the most common and costly risks.

The Rising Cost of Risk

Because vacant properties are so much riskier, finding affordable coverage is getting tougher. In 2024, the home insurance market saw premiums for new policies jump by an average of 17.4% due to industry-wide pressures. This hits high-risk vacant homes especially hard. Since 2021, some homeowners have seen their renewal costs skyrocket by as much as 69%, adding a huge burden to their annual budget. This challenging environment is exactly why a specialized vacant home policy isn't just a suggestion—it's a necessity.

The situation is even trickier in states like Florida, where market instability and major insurers leaving have shrunk the options for everyone. As we explored in our article on how an insurer leaving Florida affects the market, these regional shifts make it even more important to be proactive and find the right coverage for your empty property before it's too late.

What Vacant Home Insurance Actually Covers

It’s easy to assume that insurance for a vacant home works just like your standard homeowner's policy. But in reality, they're built on completely different foundations.

Think of your regular home insurance as a broad, "all-risk" safety net. It covers just about everything unless a specific event is excluded. This is what the industry calls an "open perils" policy.

Vacant home insurance flips that script entirely. It’s a "named perils" policy, meaning it only covers the specific risks listed in your documents. Anything not on that list isn't covered. It’s a more focused, foundational approach designed for the unique risks of an empty property.

The Foundation of Your Coverage

Most vacant home policies, often called Dwelling Property 1 (DP-1) policies, are designed to protect your physical structure from major, catastrophic events. While the exact list can vary, you'll almost always find these core protections:

- Fire and Lightning: The absolute essential. This protects the building itself from a total loss.

- Windstorm and Hail: Critical coverage for damage to the roof, siding, and windows from severe weather.

- Explosion: This covers damage from events like a natural gas explosion.

- Damage from Aircraft or Vehicles: Protects your home if it's struck by a car or plane.

These basics ensure your investment is shielded from the biggest disasters. But as you can see, this foundational coverage leaves some major gaps—especially for a house that sits empty.

A vacant home policy is a back-to-basics safety net. Its main job is to protect the structure from catastrophic loss, not cover every little thing that could go wrong. That’s why you have to know exactly which "perils" are on your list.

Customizing Your Protection with Add-Ons

The real strength of a vacant home policy is how you can customize it with endorsements. Think of these as bolt-on protections that fill in the most common gaps. You add what you need based on your property's specific situation.

For any empty property, there are two endorsements that are practically non-negotiable:

- Vandalism and Malicious Mischief: This is a must-have. It covers intentional damage like smashed windows, graffiti, or someone breaking in and destroying the interior. Without it, you're on the hook for repairs.

- Liability Coverage: Just because the house is empty doesn't mean your responsibility ends. If a delivery person, a curious neighbor, or even a trespasser gets hurt on your property, you could be sued. This endorsement protects you from those legal and medical costs.

By carefully choosing the right endorsements, you can build a homeowners insurance vacant policy that matches the real-world risks your property faces. This ensures you’re protected from the most likely threats without paying for coverage you don't need.

Finding the Right Market for Vacant Property Insurance

Shopping for vacant home insurance isn't like picking a standard policy off the shelf. It’s a completely different ballgame. The market is smaller, the rules are different, and you need to know exactly where to look to protect your empty property.

Your search will really take you down one of two main paths. Knowing the difference between them is the first and most critical step.

Admitted Carriers vs. Surplus Lines

When you start looking for coverage, you'll run into two types of insurance providers: admitted carriers and Excess and Surplus (E&S) lines carriers.

-

Admitted Carriers: These are the household names you see on TV commercials. They're licensed and heavily regulated by your state, which means their rates and policies have to get a green light from state insurance departments. A big plus is that they're backed by state guaranty funds, which step in to protect you if the company goes belly-up. The catch? Their strict rules often make them shy away from higher-risk properties—like vacant homes.

-

Excess and Surplus (E&S) Lines: This is the specialty market. Think of it as the place that covers the risks that standard insurers won’t touch. E&S carriers have a lot more freedom to set their own rates and design policies because they aren't under the same tight state regulations. This flexibility is what allows them to offer homeowners insurance vacant policies when nobody else will.

The E&S market is the insurance industry's essential safety valve. It steps in to handle unique, tricky, or high-risk situations, making sure properties like your vacant home don't have to go without coverage.

Of course, there’s a trade-off. That flexibility usually means higher premiums, and you don’t get the safety net of a state guaranty fund. But for a lot of people with empty homes, especially in high-risk areas, the E&S market isn't just an option—it's the only option.

Why the E&S Market Is Growing

In places hammered by severe weather or tangled in tough regulations, turning to the E&S market for vacant property coverage has become a major trend. It’s the only way many homeowners can find the protection they need when standard companies run for the hills.

We're seeing this play out in states like Florida, California, and Texas, where the number of E&S policies has shot up. It shows a market that's scrambling to adapt to new levels of risk. If you want a deeper dive, the 2025 home insurance report from Matic has some great insights on this shift.

This market change has real financial consequences, particularly in states where high property taxes and insurance costs are already a huge burden. If you're feeling that squeeze, you might find our guide on how Florida homeowners can reduce their property tax bills helpful. Getting smart about these specialized insurance markets is a key part of managing the total cost of owning a vacant home.

Understanding the Cost of Your Vacant Home Policy

Figuring out the price of insurance for a vacant property isn't a simple plug-and-play calculation. Insurers have to look at a unique blend of factors that go way beyond the home's value and zip code. Because an empty home is a riskier home, every single detail matters in shaping your final premium.

It all boils down to risk. An empty house is a magnet for problems that can go undetected for weeks or even months. Think about a small pipe leak that turns into a catastrophic flood, or vandals stripping copper piping from the walls. Insurers have to price that elevated risk into every policy.

As a rule of thumb, you can expect to pay 50% to 100% more for vacant home insurance than you would for a standard homeowner's policy on an occupied house.

Key Factors That Drive Your Premium

So, what exactly are insurers looking at when they calculate your rate? Several specific variables play a huge role. Knowing what they are can help you anticipate the cost and, in some cases, take steps to manage it.

The main drivers of your rate include:

- Reason for Vacancy: Why is the house empty? A property that’s staged and waiting for a quick sale is a very different risk than one undergoing a year-long gut renovation. The context is crucial.

- Duration of Vacancy: How long will it be empty? A home that will be vacant for three months is much less risky than one that will sit empty for over a year. The longer the vacancy, the higher the premium.

- Property Condition and Location: The age of the home, its current state of repair, and whether it's in a high-crime or storm-prone area will all heavily influence the final cost.

- Security Measures: This is where you have some control. A house with a monitored alarm system, security cameras, solid deadbolts, and secure fencing is a much better risk in an insurer's eyes.

An insurer's main question is always: "How likely is something to go wrong, and how bad will it be when it does?" Your policy's cost is the direct answer to that question, based on the specific details of your property.

How Your Actions Influence the Cost

Your proactive efforts can make a real difference in your premium. Insurers love to see a homeowner who takes clear, tangible steps to protect their asset. For example, hiring a property manager or asking a trusted neighbor to do regular check-ins shows responsibility and shrinks the chance of a small problem becoming a disaster.

Simple maintenance helps, too. Keeping the property’s exterior tidy, setting the heat to a minimum of 55°F in the winter to prevent frozen pipes, and even shutting off the main water supply are all smart moves that can lower your perceived risk.

These actions prove to the insurer that you're actively managing the property, not just abandoning it. That can lead directly to a more favorable rate.

While you should expect to pay more for this specialized coverage, understanding what drives the cost gives you a clearer picture. For a baseline, you can check out our guide on the average cost of homeowners insurance for occupied homes. It really highlights why the unique risks of a vacant property create a necessary price difference.

How to Get the Right Vacant Home Policy (And Keep It)

Getting the right insurance for an empty house isn't just a one-and-done deal. It's an active process of managing risk. If you have a clear game plan, you'll not only get covered but also show the insurer you're a responsible owner, which is key to keeping that coverage.

First things first, get your documents in order. Create a simple file with recent, clear photos of the inside and outside of the house. Also, list out all the security features you have—deadbolts, alarm systems, motion lights—and jot down a clear timeline for how long the property will be vacant. This prep work makes the quoting process way smoother and more accurate.

Next, you'll want to find an independent insurance agent who knows the ins and outs of vacant properties. This is a big deal. Unlike a captive agent who works for just one company, an independent agent can shop around for you. They have access to specialty carriers, often called Excess and Surplus (E&S) lines, which are frequently the only ones willing to insure a vacant home.

Your End of the Bargain: Homeowner Responsibilities

Once you have a policy, the work doesn't stop. Insurers include specific requirements, sometimes called "warranties," that you absolutely have to follow to keep your coverage valid. If you don't, you risk having a claim denied, leaving you on the hook for the entire loss.

Think of it as a partnership where your job is to actively keep risks to a minimum.

Maintaining your vacant property isn't just about keeping the neighbors happy; it's a contractual obligation. Insurers expect you to be a proactive partner in protecting the asset they've agreed to cover.

To stay on the right side of your policy, focus on these three key areas:

- Regular Check-Ins: Get a trusted neighbor, family member, or a property manager to walk through the home every week. They need to look for any signs of trouble—leaks, vandalism, or break-ins—and keep a simple log of their visits.

- Keep Utilities On: In colder climates, keep the heat set to at least 55°F to stop the pipes from freezing and bursting. Leaving the power on also runs your security system and can make the house look occupied, which deters criminals.

- Lock It Down Tight: Make sure every single window and door is securely locked. It's also smart to add motion-activated exterior lights or even a monitored security system to discourage anyone from trespassing.

The market for this kind of insurance is getting tougher. Recent analyses show that a staggering 25% of U.S. homeowners were dropped by their insurer in 2025, a sharp jump from 19% in 2024. This puts even more pressure on the already-tight vacant home market. These trends highlight why being a vigilant property manager and staying in good communication with your insurer is more critical than ever. You can discover more insights about these homeowner insurance trends and see how they're affecting vacant properties.

Common Questions About Vacant Home Insurance

When you're dealing with an empty property, a lot of specific questions pop up. It doesn't matter if you're selling a house, handling an inheritance, or just waiting on new tenants—getting the insurance details right is critical. Let's walk through some of the most common questions we hear from homeowners in this situation.

How Long Can My House Be Vacant Before My Standard Policy Is Voided?

This is the big one. Most standard homeowners policies include a "vacancy clause" that kicks in after the home has been empty for 30 to 60 consecutive days.

Once you cross that line, your coverage for some of the biggest risks—think vandalism, theft, burst pipes, and broken windows—often disappears completely. You have to read your policy or, better yet, call your agent the second you know the property will be empty. Don't ever assume you're covered.

The 30-to-60-day rule is one of the most common tripwires for denied claims. Telling your insurer before this period ends is the single best thing you can do to prevent a massive, uninsured disaster.

Is Vacant Home Insurance More Expensive?

Yes, you can bank on it. Vacant home insurance typically costs 50% to 100% more than a standard homeowners policy. The higher price tag is a direct reflection of the higher risk.

Think about it: with no one living there, a small water leak can turn into a full-blown flood before anyone notices. An empty house is also a magnet for thieves and vandals. Insurers price these policies to account for the much higher chance of a major claim.

What if My Home Is Vacant for Major Renovations?

If your house is empty because you're doing a gut renovation, a simple vacant home policy probably won't cut it. This scenario calls for a more specialized type of insurance.

You'll need to look for a "builder's risk" or "course of construction" policy. These are built from the ground up to cover the unique dangers of a construction site, including things like:

- Theft of building materials and tools

- Liability if a worker gets injured on your property

- Damage to the structure while it's being renovated

It's absolutely critical to lay out the full scope and timeline of your project for your insurance agent. They can help you figure out if you need a builder's risk policy by itself or as an add-on to your vacant home coverage.

Can I Get a Short-Term Policy?

Absolutely. Insurance companies know that vacancies are often temporary, so they offer flexible policy terms to match your needs. You can usually find vacant home policies for three, six, or twelve months.

This is perfect for common situations like:

- A house sitting on the market waiting to be sold.

- The gap between an old tenant moving out and a new one moving in.

- A short-term renovation project that requires the home to be empty.

Talk to your agent about how long you expect the vacancy to last. They can line you up with a policy that fits your timeline and explain how to extend it if things take longer than planned. This way, you only pay for the coverage you need, for as long as you need it.

At MyEasyRate Insurance, we specialize in finding the right protection for every situation, including vacant properties across South Florida. Our experienced agents can help you navigate the complexities of vacant home insurance to ensure your valuable asset is properly secured. Don't leave your empty home exposed to risk—let us help you find the peace of mind you deserve.

Get a personalized quote for your vacant property by visiting us at https://myeasyrate.com today.