When you’re looking for the best insurance companies in miami florida, you’re diving into one of the most talked-about and fastest-changing markets in the entire country. After years of sticker shock and skyrocketing rates, the landscape is finally starting to shift. New competition is moving in, and for the first time in a long while, prices are showing signs of stabilizing.

But finding the right policy here isn’t just about snagging the lowest price. It’s about partnering with a provider that’s financially solid, easy to work with when you need them, and truly understands the unique risks of South Florida living.

Understanding the Miami Insurance Market

Let’s be honest: navigating Miami’s insurance world can feel like a full-time job. For years, residents have been slammed with some of the highest premiums in the nation, making the hunt for good, affordable coverage feel almost hopeless.

But it’s not. This guide is here to cut through the noise and show you that reliable, fairly-priced insurance is actually within reach. We’ll break down what makes the Miami market tick—from hurricane risk to the new laws that are finally shaking things up—so you understand the “why” behind the prices and can make smarter choices.

A Market in Transition

The insurance story in Miami has been a rollercoaster. In 2023, homeowners felt the pain as rates jumped by an average of over 21%. But since then, things have started to level out. For 2025, Citizens Property Insurance even announced premium decreases for about 75% of homeowners in Miami-Dade County, and some major auto insurers cut their local rates by 6% to 10.5%.

What changed? A big part of it is that at least 11 new insurance companies have entered the Florida market over the last couple of years, injecting some much-needed competition. This is a huge deal.

Of course, this transition brings both opportunities and new questions. While more players can lead to better prices, the memory of major insurers leaving Florida is still fresh. It’s made a lot of people cautious and wondering about the stability of both new and old companies. If that’s on your mind, it’s worth understanding what happens when a major insurer leaves Florida and what it means for you.

The key to navigating this evolving market is empowerment through knowledge. Understanding the forces at play—from weather patterns to regulatory reforms—equips you to ask the right questions and make decisions that protect your assets without draining your finances.

The Core of Your Protection

At its heart, insurance is just a safety net for your most important stuff. In a city like Miami, where the risks run from Cat 5 hurricanes to I-95 traffic jams, having the right policies isn’t just a good idea—it’s essential.

To get you started, here’s a quick rundown of the most common types of insurance you’ll need to think about in Miami. Each one plays a specific role in shielding you from financial disaster.

Quick Guide to Common Insurance Types in Miami

| Insurance Type | Primary Purpose | Key Coverage Areas |

|---|---|---|

| Homeowners Insurance | Protects your home and belongings. | Fire, theft, windstorms, and liability if someone is injured on your property. |

| Auto Insurance | Covers car accidents and is required by law. | Liability for injuries/damage to others, plus optional collision/comprehensive coverage for your own car. |

| Flood Insurance | Covers damage specifically from rising water. | Damage from storm surge, overflowing rivers, and heavy rain accumulation. A crucial, separate policy. |

| Boat Insurance | Protects your vessel on and off the water. | Damage to the boat, liability for accidents, and coverage for equipment and trailers. |

Think of these as the building blocks. By understanding what each one does, you can start putting together a protective shield that’s perfectly suited for your life here in the Magic City.

Why Your Miami Insurance Premiums Are So High

If you’ve ever opened an insurance bill in Miami and felt that jolt of sticker shock, you’re definitely not alone. Premiums here can feel astronomically high compared to other parts of the country, leaving a lot of us wondering what’s driving these staggering costs. It’s not random; it’s a perfect storm of environmental risks and economic pressures.

Understanding what’s behind those numbers is the first step toward managing them. The high prices are a direct reflection of the very real risks that insurance companies in miami florida have to cover. Let’s break down exactly why your policy costs so much.

The Hurricane Factor and Reinsurance

The biggest driver, without a doubt, is our geography. We live in a prime location for hurricanes. When a major storm barrels through, the potential for widespread, catastrophic damage is immense, and insurers have to be ready to pay out billions in claims almost overnight.

So how do they protect themselves from going bankrupt after a monster storm? They buy their own insurance, a product called reinsurance. Think of it as a financial safety net for the insurer. When a hurricane like Andrew or Irma causes massive devastation, the reinsurer steps in to help cover those enormous losses.

But that protection isn’t cheap. Reinsurance is a global market, and as major storms get more frequent and intense worldwide, its cost goes up for everyone—especially for carriers in high-risk zones like South Florida. And where does that extra cost go? It gets passed directly to you in the form of higher premiums.

Rising Rebuilding and Litigation Costs

Beyond the storms themselves, the sheer cost to rebuild a damaged home in Miami has skyrocketed. This isn’t just simple inflation; it’s a mix of local pressures.

- Labor Shortages: Finding skilled construction labor in South Florida is tough. The workers who are available can command higher wages, which drives up the total cost of any repair job.

- Material Prices: From lumber and roofing to concrete and drywall, supply chain issues and high demand have sent the price of building materials through the roof.

- Strict Building Codes: Miami-Dade has some of the toughest building codes in the nation. While that makes our homes safer, it also makes them more expensive to repair or rebuild to meet the latest standards after a claim.

On top of all that, Florida has historically been a hotbed for insurance lawsuits. This litigious environment creates a ton of uncertainty and racks up huge legal bills for insurers, who then have to factor those potential costs into the premiums everyone pays.

“The true cost of a policy is a reflection of three things: the probability of a claim, the potential cost of that claim, and the operational expenses to manage it. In Miami, all three of those factors are amplified.”

Flood Zones and Water Risk

Another critical piece of the puzzle is Miami’s vulnerability to flooding. Here’s a crucial point many people miss: standard homeowners insurance policies do not cover damage from rising water. That’s a misconception that can be financially devastating.

Given our low elevation and proximity to the ocean, much of Miami is designated as a special flood hazard area. This means properties in these zones have a high statistical chance of flooding, making a separate flood insurance policy not just a smart move but often a requirement from your mortgage lender. The higher the flood risk for your property, the more that flood policy will cost you, adding another expensive layer to protecting your home.

This mix of factors leads to one of the heaviest insurance burdens in the country. The data is pretty stark: Miami homeowners pay roughly 19% of their mortgage bill on insurance, which is nearly double the national average of 9.7%. Florida as a whole now has the highest average home insurance cost in the nation, hitting around $14,140 in 2024. You can read the full research about these high home insurance costs and see how they stack up nationally.

Decoding Your Must-Have Coverage in Miami

Choosing the right insurance in Miami isn’t about ticking boxes on a generic form. It’s about building a practical, real-world shield against financial trouble. It’s easy to get lost in policy jargon, but what really matters is knowing your coverage will actually work when you need it most. The best insurance companies in miami florida don’t just sell policies; they help you understand exactly what you’re buying.

Think of your insurance as a specialized toolkit for Miami living. You wouldn’t use a screwdriver to hammer a nail, right? The same logic applies here—you need the right tool for each specific risk. Let’s break down the essential coverages you need in your toolkit, skipping the confusing definitions and focusing on what they do in situations you might actually face.

Homeowners Insurance: The Foundation

Your standard homeowners policy (often called an HO-3) is the bedrock of your protection. Its main job is to cover your house and belongings from common disasters like fire and theft. It also includes liability protection in case someone gets hurt on your property.

Here in Miami, this policy also covers wind damage. If a tropical storm rips shingles off your roof, that’s a standard homeowners claim. But the protection stops where the floodwaters begin.

A critical mistake Miami homeowners make is assuming their standard policy covers all water damage. Wind-driven rain coming in through a storm-damaged roof is usually covered. Rising water from a storm surge or flash flood is not.

This distinction is a big deal, and it brings us to the most vital add-on for any South Florida resident.

Flood Insurance: The Non-Negotiable Add-On

If a hurricane pushes a wall of water into your neighborhood and floods your first floor, your homeowners policy won’t pay a dime for the damage. For that, you absolutely need a separate flood insurance policy.

Given Miami’s low elevation and miles of coastline, this isn’t an optional luxury—it’s a financial necessity. And don’t think you’re safe just because you’re not in a “high-risk” flood zone. A huge number of flood claims come from areas officially rated as low-to-moderate risk after a sudden, intense downpour.

Auto Insurance: Beyond the Bare Minimum

Florida is a “no-fault” auto insurance state. This means every driver must carry Personal Injury Protection (PIP), which covers your own initial medical bills after a crash, no matter who was at fault.

But here’s the catch: the state only requires $10,000 in PIP coverage. In a serious wreck on I-95 or the Palmetto, that amount can disappear after a single trip to the emergency room. Relying on the state minimum is a massive gamble.

Here’s why you need better auto coverage in Miami:

- Bodily Injury (BI) Liability: This is crucial. It covers injuries you cause to other people if you’re at fault. Without it, you could be sued personally for their medical bills, lost income, and more.

- Uninsured/Underinsured Motorist (UM/UIM): This protects you when you’re hit by a driver with little or no insurance. It’s a sad reality that many drivers on our roads are underinsured.

- Collision and Comprehensive: Collision pays to fix your car after a crash. Comprehensive covers everything else—theft, vandalism, or a tree branch falling on your hood during a storm.

With Miami’s legendary traffic and high accident rates, skimping on auto insurance is one of the fastest ways to put your financial future at risk.

Windstorm Mitigation: The Money Saver

Finally, let’s talk about windstorm mitigation. This isn’t actually a type of insurance. It’s a way to earn serious discounts on your homeowners premium by making your house stronger against hurricanes.

When you make specific upgrades and have them certified with a wind mitigation inspection, insurers reward you with lower rates because you’re less of a risk. Common improvements include:

- Hurricane Shutters: Protecting all windows and glass doors.

- Impact-Resistant Windows/Doors: Glass built to withstand flying debris.

- Roof-to-Wall Connections: Special metal clips or straps that secure your roof to the walls.

- A Hip Roof: A pyramid-shaped roof that performs much better in high winds.

By understanding how these core coverages apply to real Miami life, you can find an insurance partner who will help you build a policy that isn’t just a piece of paper, but a reliable defense for everything you’ve worked for.

How to Choose the Right Miami Insurance Company

Picking an insurance company in Miami is a completely different ballgame. A slick TV ad or a rock-bottom initial quote tells you next to nothing about how that company will behave when a hurricane is churning offshore or you’ve got a foot of water in your living room. The best insurance companies in Miami, Florida, are the ones that are stable, responsive, and reliable when the pressure is on.

Forget the usual playbook. Finding the right partner here requires looking past the monthly premium and developing a clear framework to figure out who you can really trust. That means getting under the hood to check a company’s financial health, digging into their real-world track record with customers, and understanding exactly who you’re buying from.

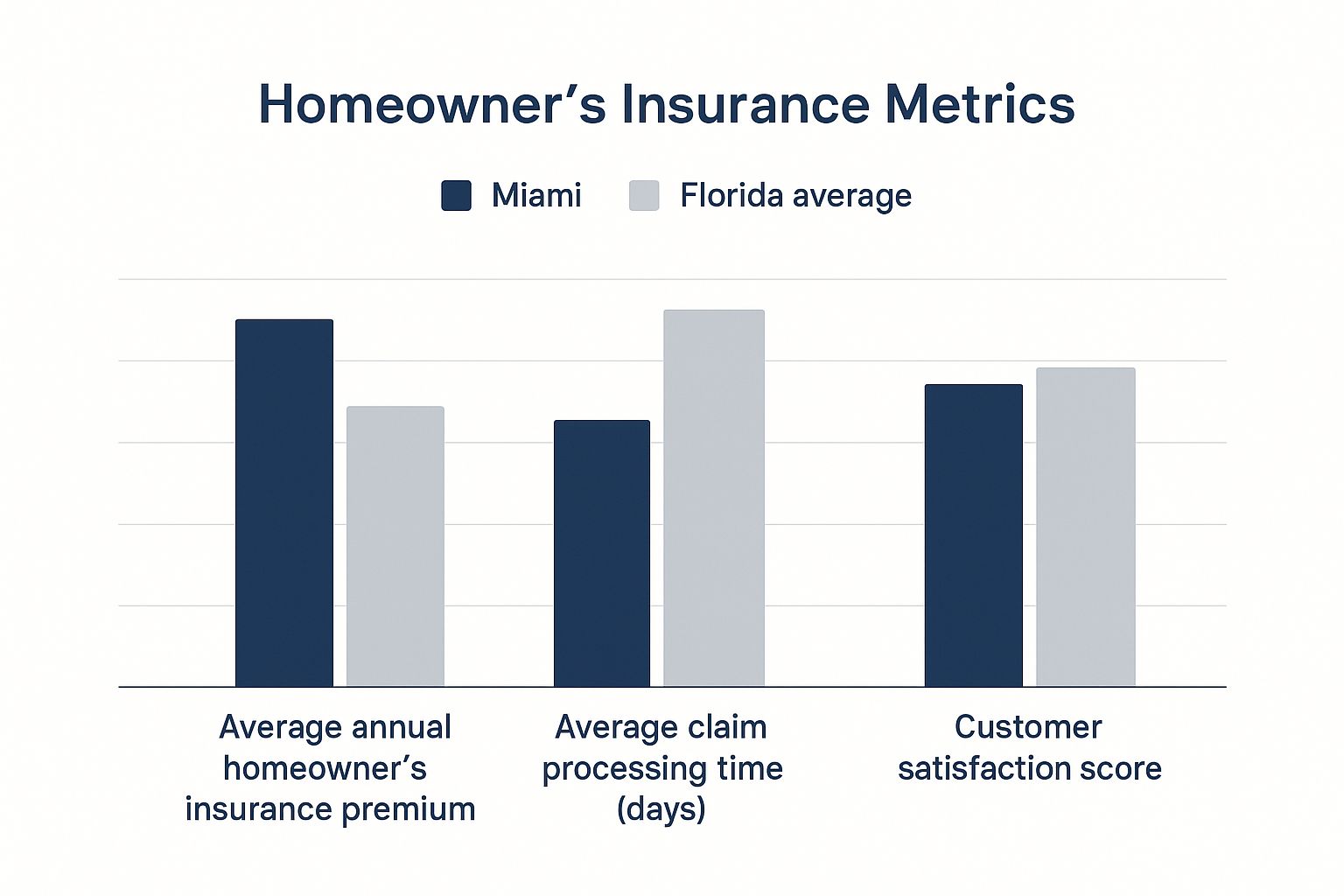

This infographic paints a pretty stark picture of the unique challenges we face in Miami compared to the rest of the state.

The data is clear: Miamians don’t just pay more for coverage; we often face longer waits and lower satisfaction. That makes your choice of insurer absolutely critical.

Evaluate Financial Stability First

Before you even glance at a quote, you need to answer one question: does this company have the financial muscle to pay out claims after a widespread disaster? Think of it like checking the foundation of a house before you buy it. A cheap policy is worthless if the company behind it goes belly-up after a major storm.

Thankfully, independent rating agencies do the heavy lifting for you. They scrutinize an insurer’s financial records and give them a grade.

- A.M. Best: This is the gold standard in the insurance world. You want to see a rating of “A-” (Excellent) or higher. It’s a strong indicator they can meet their obligations.

- Demotech, Inc.: This agency is especially important in Florida, as they specialize in rating regional insurers. A rating of “A” (Exceptional) or better is a solid sign of stability.

These ratings are public information and easy to find online. Never, ever sign a policy without first checking this out.

Investigate Their Customer Service Record

A company’s financial rating tells you if they can pay a claim. Their complaint history tells you if they will pay it fairly and without making your life miserable. This is a non-negotiable step in your research.

In a market where customer satisfaction is a major pain point, looking at complaint data isn’t just smart—it’s essential self-defense. It gives you a glimpse into the real-world experiences of other policyholders.

Recent trends in Florida are troubling. Consumer complaints about property insurance more than doubled from 10,219 in 2020 to over 23,400 in 2024. To put that in perspective, one company, Universal Property & Casualty, racked up around 16,170 complaints in just five years—more than even the state’s largest insurer. You can get a better sense of these complaint trends for Florida insurers and see how different companies compare.

Understand Who You Are Buying From

Finally, it’s crucial to know who you’re dealing with. An “insurance agent” and an “insurance broker” sound similar, but the difference can have a massive impact on your options and the quality of advice you receive.

Knowing which type of insurance professional to work with is a key part of the process. Each model has its benefits and drawbacks, depending on your needs.

Comparing Insurance Provider Types in Miami

| Provider Type | Pros | Cons | Best For… |

|---|---|---|---|

| Captive Agent | Deep product knowledge of one company; streamlined process. | Can only offer products from their single employer (e.g., State Farm, Allstate). | Customers loyal to a specific brand or those with simple, straightforward insurance needs. |

| Independent Agent/Broker | Represents multiple insurance companies; can shop the market for you. | May not have the same level of in-depth knowledge of every single carrier. | Anyone with complex needs or who wants to compare multiple options to find the best value in a tough market like Miami. |

So, what does this all mean for you?

A captive agent works for one specific company. They know that company’s products inside and out, but they can’t sell you anything else.

An independent agent or broker, on the other hand, works for you. They have access to multiple carriers and can shop around on your behalf to find the best fit for your unique situation.

In a complex, expensive, and constantly shifting market like Miami, an independent professional gives you a huge advantage. They bring more choices to the table and provide unbiased advice, helping you find a true partner, not just a policy.

Proven Strategies to Lower Your Insurance Costs

Once you’ve found a solid, reputable provider, the next move is making sure you aren’t overpaying. High premiums are a fact of life in South Florida, but they aren’t carved in stone. You have more control over what you pay than you might think. It just takes being proactive.

Putting even a couple of these tactics to work can lead to real savings on your policies from even the best insurance companies in Miami Florida. This isn’t about cutting corners on coverage you need; it’s about smart management to lock in the best possible rate.

Fortify Your Home for Big Discounts

One of the most powerful ways to slash your homeowners insurance is through windstorm mitigation. Insurers give major discounts to homeowners who beef up their properties against hurricane damage. Why? Because it lowers their risk of a massive payout.

Making these upgrades—and getting them certified by a licensed inspector—unlocks some of the biggest savings you can get.

- Install Hurricane Shutters or Impact Glass: Protecting your windows and doors is your first line of defense against wind and flying debris.

- Strengthen Your Roof: This means using stronger roof-to-wall connectors (often called hurricane clips), improving how the roof deck is attached, and adding a secondary water-resistant layer underneath.

- Upgrade Your Garage Door: A wind-rated garage door is critical. If it fails, the pressure change inside your home can be catastrophic during a storm.

Yes, these improvements are an upfront cost, but the annual premium savings can be so significant they often pay for the upgrades over time.

Bundle Policies and Adjust Deductibles

Another simple strategy is bundling. Most insurers offer a multi-policy discount when you buy more than one policy from them, like home and auto. That discount often lands between 10% and 20%, an easy win for trimming your total insurance bill.

You can also tweak your deductibles. Your deductible is what you pay out-of-pocket on a claim before your insurance coverage starts paying.

Raising your deductible from $1,000 to $2,500 can lower your homeowners premium by hundreds of dollars a year. The logic is straightforward: when you agree to cover a larger chunk of a potential small loss yourself, the insurance company rewards you with a lower premium.

Just make sure you pick a deductible you can comfortably pay on short notice. Don’t set yourself up for a financial struggle if you need to file a claim.

Maintain Good Credit and Review Annually

Here’s something many people don’t realize: insurance companies often use a credit-based insurance score to help set your premiums. This practice is banned in some states, but it’s fair game in Florida. Statistically, people with higher credit scores tend to file fewer claims. By maintaining a good credit history, you can position yourself for better rates on both your home and auto policies.

Finally, don’t just “set it and forget it.” Your life changes, and so do your insurance needs. An annual policy review with your agent is essential. It’s your chance to discuss any updates, confirm your coverage is still right for you, and—most importantly—ask if there are any new discounts you now qualify for.

For car owners, there are a ton of other ways to bring down that monthly payment. For a deeper dive, check out our guide on how to lower car insurance costs for more tips you can use today. By actively managing your policies and taking these concrete steps, you can make a serious dent in what you pay for insurance.

Your Action Plan for Finding the Best Coverage

Alright, let’s bring this all home. You’ve waded through the complexities of Miami insurance, and now it’s time to turn that knowledge into action. Think of this as your final checklist—a clear, step-by-step game plan to lock in the right protection for your family and assets in the South Florida market.

The whole process starts with an honest look in the mirror at what you truly need to protect. What are your biggest risks? From there, it’s all about doing your homework on the insurance companies in miami florida that are financially solid and treat their customers right. Don’t gloss over this part; a cheap policy from a shaky company is a gamble you can’t afford to lose when a storm hits.

Your Step-By-Step Checklist

- Define Your Needs: First things first, make a simple list of everything you need to insure—your house, your cars, and your personal liability. Make sure to factor in Miami-specific risks like flooding and hurricanes right from the get-go. This ensures you’re asking for the right kind of quotes from the start.

- Research Insurers: Before you even talk to an agent, look up the financial ratings from A.M. Best and Demotech for any company on your shortlist. After that, a quick check of their customer complaint history with state regulators will tell you a lot about how they handle claims.

- Gather Multiple Quotes: Aim to get quotes from at least three different providers. Make sure one of them is an independent agent who can shop the entire market for you. This is the only real way to know if the price you’re being offered is competitive.

- Compare Apples-to-Apples: When the quotes start rolling in, line them up side-by-side. Check that the coverage limits, deductibles, and policy terms are identical. This is crucial for making an honest comparison of value, not just chasing the lowest price tag.

Remember, the goal isn’t just to find a policy, but to find a reliable partner. The right insurer will be there to support you when you need them most, making the research phase a critical investment in your peace of mind.

Once you’ve got your quotes and have a good feeling about the companies, the last step is to read the actual policy documents before signing anything. Pay close attention to the fine print on exclusions and any special add-ons (endorsements). For instance, understanding exactly what you’re responsible for is key. That’s why we always point out the importance of protecting your belongings and why renters insurance matters—it’s a perfect example of how crucial personal property coverage is.

By following this straightforward approach, you put yourself in the driver’s seat. You’ll go from being a passive buyer to a smart consumer who’s ready to secure the best protection Miami has to offer.

Miami Insurance FAQs: Your Top Questions Answered

Getting your head around insurance in Miami can feel like a maze. Let’s cut through the noise and tackle some of the most common questions we hear from residents every single day.

Do I Really Need Flood Insurance if I’m Not in a High-Risk Zone?

Yes, absolutely. This is one of the most critical and misunderstood parts of protecting a Miami property.

A standard homeowners policy will never cover damage from rising water—what insurers define as a flood. Think storm surges, overflowing canals, or even torrential rain that pools and seeps into your home from the ground up. In Miami, with our low elevation and frequent downpours, this happens all the time, well outside the “official” high-risk flood zones.

In fact, a huge percentage of flood claims across the country come from properties in supposedly low-risk areas. A separate flood policy is the only way to protect yourself.

Here’s a simple way to think about it: Your home insurance covers water falling down (like rain through a damaged roof). Flood insurance covers water rising up. In a city like ours, you absolutely need both.

What’s the Difference Between a Captive Agent and an Independent Broker?

Knowing this can completely change your insurance-buying experience. The core difference is who they work for.

A captive agent works for one company and one company only, like State Farm or Allstate. They’re an expert on that company’s products, but they can only sell you what that single carrier offers.

An independent insurance broker, on the other hand, works for you. They aren’t tied to any single insurer. Instead, they partner with many different carriers and can shop the entire market to find the right fit and price for your specific situation. For a complicated market like Miami, an independent broker gives you far more options and leverage.

My Insurer Is Dropping My Policy. What Now?

First, take a breath. It’s a stressful situation, but it has become incredibly common for homeowners all over Florida. The good news is your insurer must give you advance notice, which gives you a window to find a new policy.

Here’s your game plan:

- Start Shopping Immediately: Don’t wait. Use that notice period to get ahead of the deadline and start looking for new coverage.

- Call an Independent Agent: This is your best first move. An independent agent can quickly check rates with multiple carriers, including newer insurance companies in miami florida that are hungry for new business.

- Know Your Last Resort: If the private market turns up nothing, your final option is Citizens Property Insurance Corp., Florida’s state-backed insurer. It’s there as a safety net.

The key is to act fast. You don’t want even a single day’s lapse in coverage for your biggest asset.

Tackling these challenges is much easier when you have an expert on your side. The team at MyEasyRate Insurance lives and breathes the South Florida market. We can help you find the right policy from a top-rated carrier. Visit us at https://myeasyrate.com to get a free, no-hassle quote today.

Article created using Outrank