To get a handle on car insurance rates in Florida, you first have to accept one hard truth: our market is uniquely expensive. Florida drivers consistently pay some of the highest premiums in the nation. Because of that, using a comparison tool to see multiple quotes at once isn't just a good idea—it's the single best strategy to find affordable coverage and stop yourself from overpaying.

Why Florida Car Insurance Rates Are So High

If you've ever looked at your car insurance bill and thought it seemed way too high, you're not imagining things. The Sunshine State is one of the most expensive places in the country for auto coverage, which makes finding a fair price a real challenge for drivers here.

This reality makes it crucial to compare car insurance rates in Florida, but understanding why they’re so high is the first step toward finding better value. It all comes down to a few distinct factors that drive up costs for everyone. Insurers pay out more in claims here, and they pass those costs right back to us through higher premiums.

The Perfect Storm of Rate Factors

The high cost isn't because of one single issue. It’s a combination of persistent problems that define the Florida insurance market, and each one adds another layer of expense that ultimately hits your wallet.

The key drivers behind Florida's expensive premiums are:

- Severe Weather Events: Florida's constant exposure to hurricanes and tropical storms means a massive number of comprehensive claims for flood and wind damage. This dramatically increases the risk for insurers.

- High Litigation Costs: For years, the state has been a hotspot for auto insurance lawsuits and fraudulent claims, which inflates operating costs for every insurance company.

- Uninsured Drivers: Florida has one of the highest rates of uninsured motorists in the entire country. When an uninsured driver causes a wreck, the costs often get absorbed by insured drivers' policies, pushing everyone's rates up.

Florida historically has the highest car insurance rates in the United States, with the average full coverage premium hitting $4,171 annually in 2023. That's about 58% higher than the national average.

While rates skyrocketed in recent years, some major insurers did start to slightly reduce them in 2024. But don't get too excited—even with these small adjustments, Florida's auto premiums are still the costliest in the nation. This complex and expensive environment makes proactive shopping not just a smart move, but a necessary one for keeping your budget in check.

Key Factors That Influence Your Insurance Premium

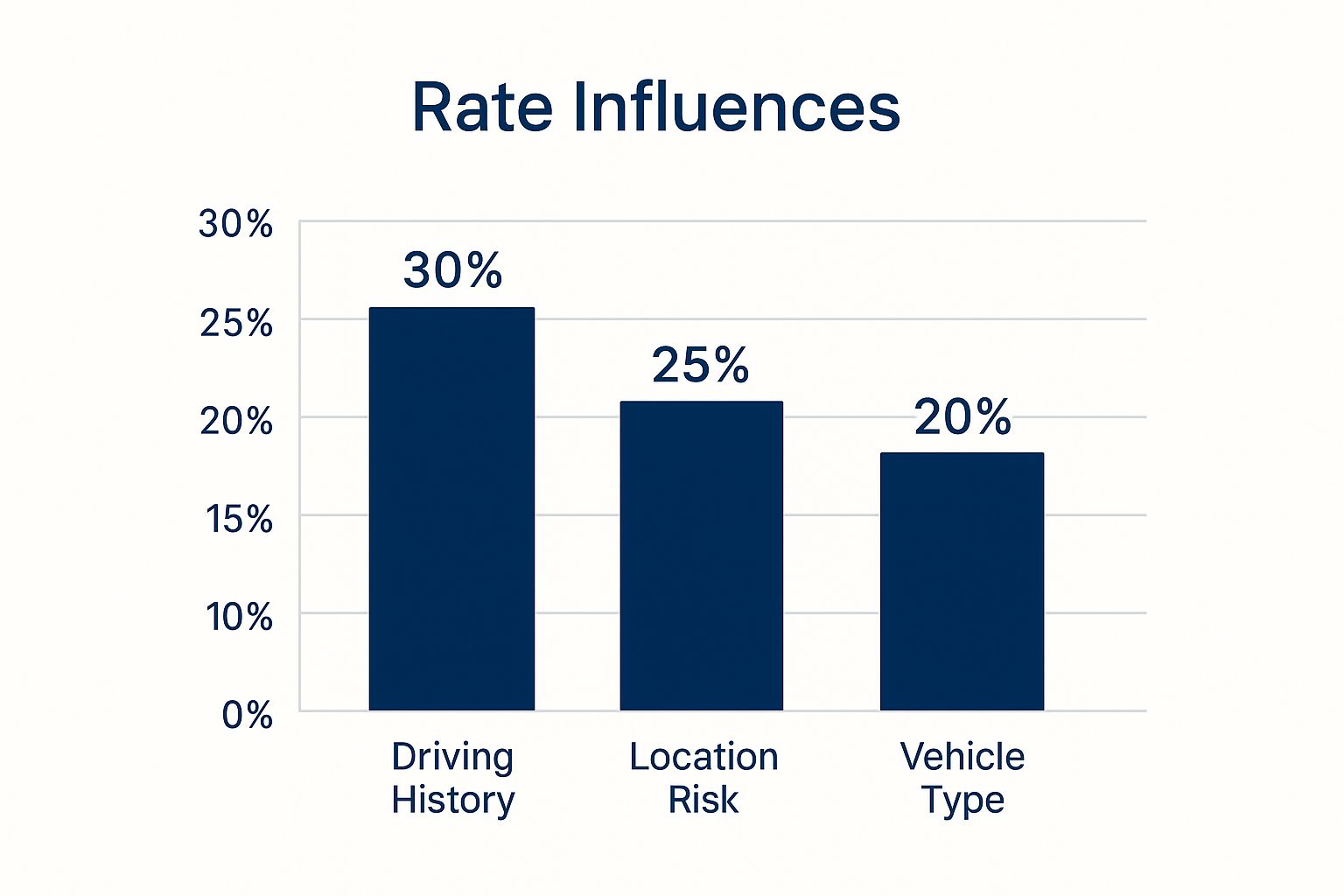

When an insurer calculates your car insurance quote, they're not just guessing. They're using a complex recipe of data points to build your unique risk profile. While obvious things like your driving record and the type of car you own are huge ingredients, a bunch of other personal details play a major role in what you'll actually pay.

Getting a handle on these variables is the first step toward finding ways to trim your costs. Insurers in Florida look at everything from your ZIP code to your credit history to figure out the odds of you filing a claim. Each company weighs these factors differently, which is why quotes can be all over the map.

This image breaks down the main categories that shape your insurance bill.

As you can see, your driving history is king, but where you live and what you drive are right behind it in importance.

Your Location and Mileage

Where you park your car at night has a massive impact on your rates here in Florida. Insurers analyze risk right down to the ZIP code, looking at local stats for theft, vandalism, and how often accidents happen. It's no surprise that a driver in a packed urban area like Miami will almost always pay more than someone in a quiet, rural town.

How much you drive also matters. The more time you spend on the road, the higher the statistical chance of getting into an accident. If you have a long daily commute, your premium will reflect that extra risk compared to someone who works from home or rarely drives.

Personal and Financial Profile

Your personal details are just as critical as your driving habits. Insurers consider several non-driving factors when setting your premium, including:

- Credit History: In Florida, insurers are allowed to use a credit-based insurance score to help set rates. Statistically, people with higher credit scores tend to file fewer claims. It's a controversial but legal practice.

- Marital Status: Married couples are often seen as more stable and less risky by insurance models, which can lead to slightly lower premiums compared to single drivers.

- Age and Gender: This is a big one. Younger, less experienced drivers—especially males under 25—typically face the highest rates because, statistically, they're involved in more accidents.

To see how this plays out with real numbers, let's look at how different personal factors can swing a baseline premium.

How Personal Factors Impact Your Annual Premium in Florida

| Influencing Factor | Scenario | Estimated Premium Impact (Annual) |

|---|---|---|

| Baseline (Good Driver) | 40-year-old, married, good credit | $4,143 |

| Age | 20-year-old single male | Add +$2,500 to +$4,000 |

| Credit Score | Poor credit vs. excellent credit | Add +$1,500 to +$3,000 |

| Driving Record | One at-fault accident | Add +$1,200 to +$2,000 |

| Location | Miami (33130) vs. Gainesville (32601) | Add +$800 to +$1,500 |

| Marital Status | Single vs. Married | Add +$150 to +$300 |

Disclaimer: These are simplified estimates for illustrative purposes. Your actual premium will vary based on the insurer and your complete profile.

As the table shows, factors like your age and credit score can have an even bigger financial impact than a fender bender.

Your Vehicle and Coverage Choices

The car you drive is another major piece of the pricing puzzle. A high-performance sports car or a luxury SUV with expensive-to-replace parts is going to cost more to insure than a basic, reliable sedan. Insurers look up repair costs, theft rates, and safety ratings for your specific make and model.

Of course, the coverage levels you choose directly affect your bill. While just getting Florida's minimum required coverage is the cheapest option, it can leave you dangerously exposed financially if a serious accident happens. It's all about striking the right balance between cost and protection.

For more specific strategies, check out our guide on how to lower your car insurance costs. By understanding exactly what insurers are looking at, you can make smarter decisions that lead to much more affordable coverage.

A Practical Guide to Comparing Quotes Accurately

Getting accurate online insurance quotes requires a little prep work and a clear strategy. To really compare car insurance rates in Florida efficiently, you need more than just your name and address. A few key documents will make the whole process faster and way less frustrating.

Before you even start clicking, pull together the essential info for every driver you plan to put on the policy. Trust me, this simple step saves you from scrambling to find documents halfway through a quote.

Prepare Your Information

To get quotes you can actually trust, you have to feed every company the exact same details. Having this stuff ready to go ensures each insurer is working with the same data, which is critical.

- Driver’s License Numbers: You'll need the license number for every driver in the house who will be on the policy.

- Vehicle Identification Numbers (VINs): Grab the VIN for each car you want to insure. You can usually find it on your dashboard (driver's side, near the windshield), the driver's side doorjamb, or your current insurance card.

- Current Policy Details: Keep your current insurance policy’s declarations page handy. This is your cheat sheet—it lists your existing coverage limits and deductibles, which you'll want to match for a true comparison.

Once you have this info, you’re ready for the most important part of the process: making sure every quote is built on the same foundation.

The single biggest mistake shoppers make is comparing quotes with different coverage levels. A policy with low liability limits will always look cheaper than one with robust protection, but it's a misleading comparison that could leave you financially exposed.

Ensure an Apples-to-Apples Comparison

The goal isn’t just to find the lowest number. It’s to find the best price for the exact same coverage. To do that, you have to standardize the details across every single quote you request. It's the only way to know which company is truly offering you a better deal.

Focus on matching these three core components perfectly:

- Coverage Limits: If you're quoting $100,000/$300,000 in bodily injury liability with one insurer, you must use those same limits with all the others.

- Deductibles: Your comprehensive and collision deductibles (whether it's $500 or $1,000) have to be identical in every quote. A lower deductible will always mean a higher premium.

- Endorsements and Add-Ons: Make sure you're including (or excluding) the same optional coverages, like rental reimbursement or roadside assistance, in each quote.

When the quotes start rolling in, organize them in a simple spreadsheet. Make columns for the insurance company, the six-month premium, the annual premium, and each type of coverage. This kind of clean, visual layout makes it incredibly easy to spot the most cost-effective option for the protection you actually need.

How to Interpret and Analyze Your Insurance Quotes

Getting a bunch of car insurance quotes is the easy part. The real work is figuring out what those numbers actually mean. When you compare car insurance rates in Florida, you have to look past the premium and see the full picture—a quote is a detailed breakdown of your financial protection, not just a price tag.

Let’s be blunt: the lowest price is almost never the best value, especially in a state like Florida where accidents are frequent and expensive. A suspiciously cheap premium is usually a red flag for dangerously low coverage limits, sky-high deductibles, or missing protections that you'll desperately need after a crash.

Deconstructing Your Florida Insurance Quote

At first glance, an insurance quote can feel like a jumble of industry jargon and numbers. But it’s really just organized into specific buckets that define what the insurer will (and won’t) cover if you get into an accident.

To do a true apples-to-apples comparison, you have to focus on these four critical coverages in every Florida auto quote:

- Bodily Injury (BI) Liability: This is the big one. It covers injuries or death to other people if you cause the accident. Florida doesn't require it to register your car, but driving without it is a massive financial gamble.

- Property Damage (PD) Liability: This pays for damage you cause to someone else's car, fence, or other property. The state minimum is only $10,000, an amount that a fender bender with a new truck can easily blow past.

- Personal Injury Protection (PIP): As a no-fault state, Florida requires $10,000 in PIP. This covers 80% of your own initial medical bills, no matter who was at fault. It’s your first line of defense.

- Uninsured/Underinsured Motorist (UM/UIM): This is your shield against the huge number of Florida drivers with no insurance or not enough to cover your medical bills if they hit you. Don't skip it.

The real risk isn’t the monthly premium. It’s the gap between what Florida requires and what a serious accident actually costs. A single collision can easily rack up over $100,000 in medical bills and legal fees, and if your policy is too small, you're on the hook for the rest.

The True Cost of Being Underinsured

To see why the "cheapest" quote can be the most expensive mistake you'll ever make, let's walk through a common accident scenario. Imagine you cause a wreck that leaves the other driver with $50,000 in medical bills and does $25,000 in damage to their car.

Here’s how two different policies would handle it:

Quote Analysis A vs. B

| Coverage Detail | Quote A (The Cheap One) | Quote B (Smart Protection) |

|---|---|---|

| Bodily Injury Liability | $10,000 / $20,000 | $100,000 / $300,000 |

| Property Damage Liability | $10,000 | $50,000 |

| Uninsured Motorist | Declined | $100,000 / $300,000 |

| Annual Premium | $1,900 | $2,600 |

With Quote A, your policy pays its limits and stops. That’s $10,000 for the other driver's injuries and $10,000 for their car. You are now personally on the hook for the remaining $55,000. That kind of debt can lead to lawsuits, wage garnishment, and losing your assets.

With Quote B, your policy covers the entire $75,000 cost. That extra $700 a year in premium just saved you from a lifetime of debt. This is exactly why a detailed analysis is non-negotiable when you compare car insurance rates in Florida—it’s about balancing what you pay today with protecting everything you have tomorrow.

Finding Savings Through Discounts and Market Changes

Once you’ve got a few comparable quotes lined up, the real work begins: hunting down every last discount you qualify for. Most people know about the big ones, like bundling home and auto, but carriers have dozens of other savings opportunities that often go completely overlooked.

Not asking about them is like leaving cash on the table. When you're comparing car insurance rates in Florida, you need to be proactive and ask each company for a full rundown of their discounts. Those small savings really do add up.

Common Discounts You Should Never Miss

These are the foundational savings every Florida driver should check for. Before you sign on the dotted line, make sure you've confirmed your eligibility for these heavy hitters.

- Good Driver Discount: This is your reward for staying out of trouble. Insurers typically offer this if you've had no at-fault accidents or major tickets for three to five years.

- Multi-Policy Discount: Often called "bundling," this is one of the easiest ways to get a big price break. Insuring your car and home (or renters) with the same company can often save you 10-25%.

- Multi-Car Discount: If you have more than one vehicle on the same policy, you’ll almost always get a significant discount.

- Good Student Discount: For high school or college students who keep their grades up—usually a "B" average or better.

Don't ever assume a discount will be applied automatically. Always ask your agent to walk you through exactly which savings you’re getting. A quick five-minute chat could easily uncover hundreds of dollars in annual savings.

Top Car Insurance Discounts for Florida Drivers

Beyond the basics, many Florida insurers offer a wide range of discounts that cater to specific lifestyles and choices. Here’s a quick comparison of some common (and not-so-common) ways to save.

| Discount Type | Typical Savings Range | Who Qualifies | Key Considerations |

|---|---|---|---|

| Defensive Driving Course | 5-10% | Drivers (often 55+) who complete an approved course. | Ensure the course is state-approved and recognized by your insurer before you sign up. |

| Telematics/Usage-Based | 5-30% | Safe drivers willing to use a monitoring app or device. | Savings depend on your actual driving habits (braking, mileage, time of day). Risky driving can sometimes increase rates. |

| Low Mileage | 3-15% | People who drive less than a set annual mileage (e.g., 7,500 miles). | Perfect for remote workers or retirees. You may need to provide odometer readings. |

| Paperless Billing/Auto-Pay | 2-5% | Anyone who enrolls in electronic statements and automatic payments. | This is an easy win. Just set it and forget it for a small but consistent discount. |

| Vehicle Safety Features | 5-25% | Drivers with cars equipped with anti-lock brakes, airbags, anti-theft systems, etc. | Savings vary by feature. Most modern cars will qualify for at least some of these. |

| Loyalty Discount | 5-15% | Policyholders who stay with the same insurer for several years. | The discount often increases over time, but always compare rates—loyalty doesn't always beat a competitor's price. |

Taking the time to review this list and ask your potential insurer about each one can make a huge difference in your final premium.

Unlocking Savings with Market Competition

The good news for Florida drivers? The insurance market is finally getting more competitive. After years of brutal rate hikes, we're starting to see signs of stabilization, driven by recent legislative reforms and new companies entering the state.

This shift is creating more options and putting downward pressure on prices. In fact, Florida’s top insurers have forecasted an average premium drop of 6.5% for 2025—a massive reversal from recent trends. This is happening because 11 new companies have jumped into the market, forcing everyone to compete harder for your business.

This increased competition is especially helpful in pricier metro areas. For more targeted advice, check out our guide on finding cheap auto insurance in Fort Lauderdale. In this changing market, being an informed, aggressive shopper is your best bet for landing truly affordable coverage.

Common Questions About Comparing Florida Car Insurance

Digging into the world of car insurance can feel like opening a can of worms. You’ve got questions, and you need straight answers, especially when you’re trying to compare rates here in Florida. Let's tackle some of the most common ones that pop up so you can shop with confidence.

How Often Should I Compare Car Insurance Rates?

You should never get too comfortable with your current car insurance rate. The Florida market is always in motion—new companies show up, and the ones you know are constantly tweaking how they price their policies.

As a rule of thumb, shop for new quotes at least once a year. It’s also a smart move to compare rates anytime a major life event happens, since these changes can have a huge impact on what you pay.

Think of these moments as a green light to re-shop your insurance:

- When your policy is up for renewal: Never just let it auto-renew. See what else is out there first.

- Buying a new car: The make and model you drive is a massive factor in your premium.

- Moving to a new address: Just changing your ZIP code can send your rates up or down.

- Getting married or adding a driver: Any change to your household or marital status will absolutely affect your rate.

- A shift in your driving habits: If you suddenly start working from home, your lower mileage could unlock some serious savings.

Will Getting Multiple Quotes Hurt My Credit Score?

This is a big one, but you can relax. When you ask for a car insurance quote, the insurer does what's called a "soft pull" or "soft inquiry" on your credit history.

Unlike a "hard pull" (which happens when you apply for a new credit card or a loan), a soft inquiry is only visible to you. It has zero effect on your credit score. You can get dozens of quotes from different companies without worrying about a single point dropping from your rating.

Go ahead and shop for insurance as much as you need to. The credit reporting system is designed to let people compare rates for services like this without penalizing them for being a smart consumer.

What Is the Minimum Car Insurance Required in Florida?

Florida’s insurance laws are a bit unique. To legally register and drive your car in the state, you have to carry at least two specific types of coverage.

Here are the state-mandated minimums:

- $10,000 in Personal Injury Protection (PIP): This is the core of Florida's "no-fault" system. It covers your own initial medical bills after a crash, no matter who was at fault.

- $10,000 in Property Damage Liability (PDL): This pays for the damage you cause to someone else's car or property if you're the one at fault.

Let's be clear: these minimums offer very, very little real-world protection. A simple fender bender can easily blow past these limits, leaving you on the hook for thousands of dollars out of your own pocket. Every expert will tell you to buy much higher liability limits to protect your savings and assets. Also, these requirements can sometimes vary by residency status, a key detail we cover in our guide on car insurance for undocumented immigrants in Florida.

Ready to see how much you could actually be saving? At MyEasyRate Insurance, we make it painless to compare quotes from top Florida insurers in just a few minutes. Get your free, no-pressure comparison today and find the right coverage at the right price.