Finding cheap auto insurance in Fort Lauderdale isn't a myth, but it does take a little strategy. The good news? It's entirely possible.

Right now, GEICO is often the front-runner for minimum coverage, with rates hovering around $68 per month, while Travelers frequently comes in as the most budget-friendly for full coverage plans. The key is knowing that the rates you'll see are shaped by factors unique to our corner of Broward County.

Finding Affordable Fort Lauderdale Auto Insurance

Let's be honest: shopping for car insurance in Fort Lauderdale can feel like a chore. Between the daily grind on I-95 and the ever-present risk of storm claims, our premiums are often a bit steeper than in other parts of Florida.

But here’s the upside: the local insurance scene is incredibly competitive. That competition means prices can swing wildly from one company to the next, which is fantastic news for you. A little bit of smart shopping can genuinely lead to big savings—sometimes hundreds of dollars a year.

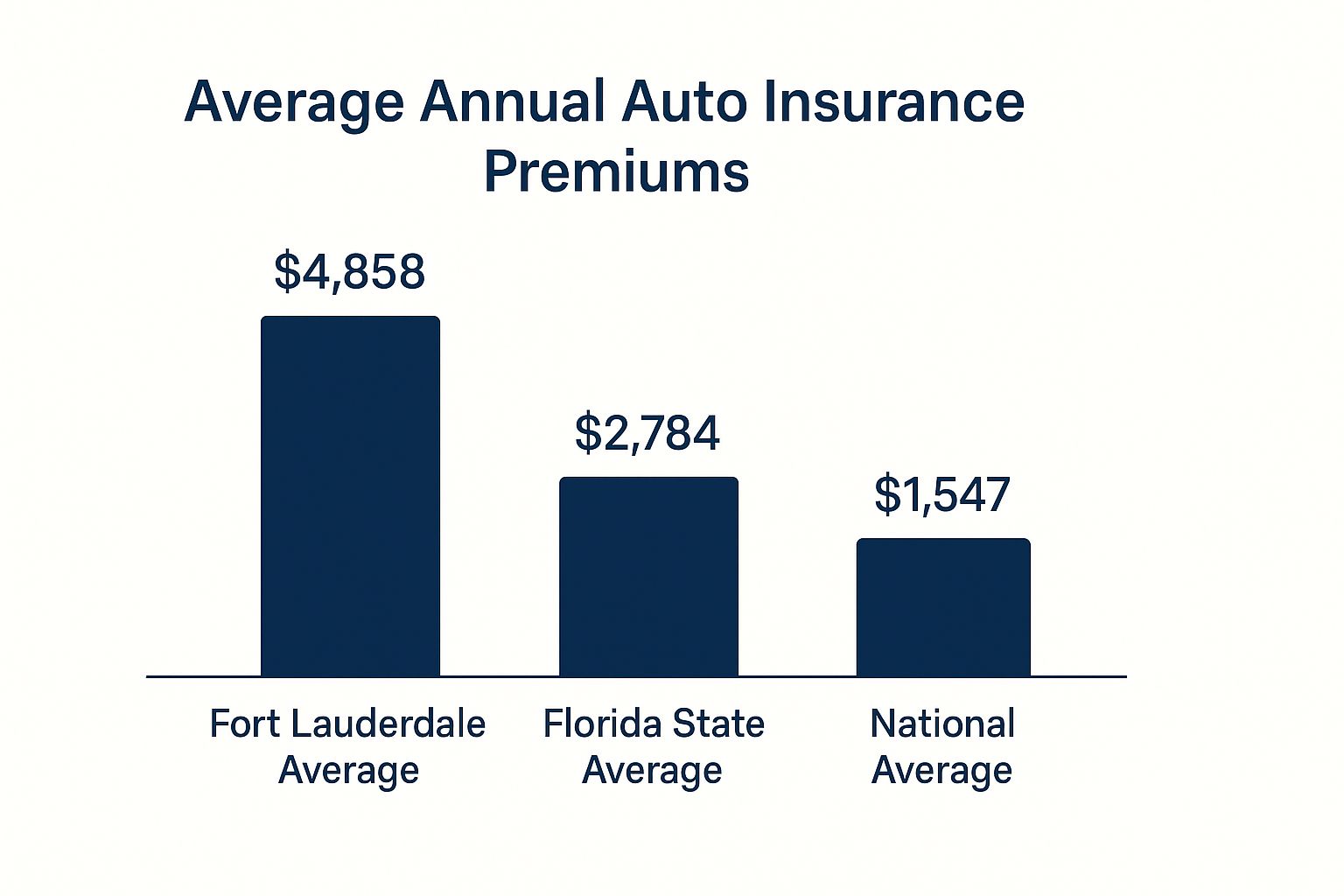

Comparing Local and National Averages

To really get a grip on what you should be paying, it helps to see how Fort Lauderdale stacks up against the rest of the state and the country. This chart paints a clear picture of the average annual costs and really drives home why finding those affordable options is so important for local drivers.

As you can see, our local premiums are noticeably higher, making it a top priority to hunt down the best possible deal.

Pinpointing the Top Affordable Insurers

So, who's offering the best rates right now? Data from early 2025 gives us a pretty clear picture.

To give you a head start, here’s a quick look at the most affordable insurance providers in Fort Lauderdale for both minimum and full coverage options. This should help you identify the top contenders right off the bat.

Fort Lauderdale's Most Affordable Auto Insurance Providers

| Coverage Type | Most Affordable Provider | Average Monthly Premium | Average Annual Premium |

|---|---|---|---|

| Minimum Coverage | GEICO | $68 | $816 |

| Full Coverage | Travelers | $155 | $1,870 |

This table provides a snapshot, but it’s always smart to get personalized quotes to see what these—and other—insurers can offer you.

For drivers just needing basic liability, GEICO is consistently the most competitive, averaging about $68 per month ($816 annually).

If you’re looking for the peace of mind that comes with comprehensive protection, Travelers is tough to beat. They're offering full coverage rates around $155 monthly ($1,870 per year). Of course, other big names like State Farm and Allstate are in the mix with competitive full coverage plans, though their average premiums tend to be a little higher.

This is exactly why comparing quotes is so crucial. We've seen Fort Lauderdale drivers save an average of $600 a year just by making the switch. If you want to dig deeper, you can explore more about these rates and see how they're calculated by checking out recent insurance studies.

How Your Fort Lauderdale ZIP Code Impacts Rates

Ever wonder why your auto insurance quote is so different from a friend's who lives just a few miles away? A huge piece of the puzzle is your ZIP code. Insurers are experts at assessing risk, and they drill down to the neighborhood level to figure out the real-world chances of you filing a claim.

Your specific address in Fort Lauderdale tells an insurance company a story. It’s a story built on hard data, not just assumptions about the city.

What Insurers Are Looking At in Your Area

When you pop your ZIP code into a quote tool, insurers instantly pull up a ton of hyper-local stats. They aren’t just looking at Fort Lauderdale as a whole; they're analyzing the unique DNA of your specific neighborhood.

Here’s what’s on their checklist:

- Accident Frequency: Some intersections and roadways are just plain notorious for crashes. Living near a high-risk area like the stretch of NW 9th Avenue and W Commercial Boulevard, which saw 244 crashes between 2023 and 2024, can nudge your premium upward.

- Theft and Vandalism Rates: Carriers track neighborhood crime data very closely. If your area has higher rates of car theft or break-ins, that directly translates to a greater risk for them paying out comprehensive claims.

- Traffic Density: It’s simple math. Areas with heavy commuter traffic—like those near downtown or major arteries like I-95—tend to have more fender-benders, leading to higher insurance costs for the folks who live there.

- Road Conditions: Believe it or not, even things like constant construction projects or poorly maintained streets in your ZIP code can be factored in, as they often contribute to more incidents.

This granular, block-by-block approach is exactly why finding cheap auto insurance in Fort Lauderdale requires a localized game plan. A driver in a quiet, residential pocket of the city will almost always pay less than someone living near a bustling commercial district.

The Real Cost Difference Across Town

The financial hit from these ZIP code ratings is no joke. The median annual auto insurance rate in Fort Lauderdale hovers around $4,859, which is roughly 20% higher than the Florida statewide average. That gap is mostly driven by our city’s dense traffic and unique weather risks.

But the price swings within the city are even more dramatic. For instance, a driver in the 33312 ZIP code might see an average monthly premium around $393. Meanwhile, someone just a short drive away in 33308 could pay as little as $111. You can dig into more of these localized rate differences in a recent Fort Lauderdale insurance data study.

Key Takeaway: Your address is one of the most powerful, non-negotiable factors in your insurance premium. While you can't just pick up and move to save money, you can switch to an insurer that views your neighborhood's risk more favorably. This is exactly why comparing quotes from multiple carriers is absolutely essential for every Fort Lauderdale driver.

Your Driving Profile Is the Real MVP for Premiums

While your Fort Lauderdale ZIP code gives insurers a starting point, your personal driving profile is what truly dictates your final rate. Insurance companies are playing a game of risk assessment, and your history behind the wheel—along with factors like your age and credit history—is their most important scorecard.

Think of it this way: a clean, responsible profile tells an insurer you're a safe bet. And they reward safe bets with their best prices.

How Age and Experience Reshape Your Rates

There's no sugarcoating it—age is a massive factor. Statistically, younger drivers are simply involved in more accidents, which is why finding cheap auto insurance in Fort Lauderdale as a teen can feel like an impossible task. They face the steepest premiums right out of the gate.

The good news? This gets better, and faster than you might think. Every year you drive without an incident, your rates should drop.

Data for 2025 paints a clear picture. Teenage drivers in Fort Lauderdale are looking at average monthly costs around $395. Once they hit their 20s, that average falls to $294. By the time drivers are in their 30s, that same policy could be as low as $89 per month with a carrier like State Farm. You can dig deeper into local data on how age and incidents impact Fort Lauderdale rates to see the trends for yourself.

The Heavy Price of a Blemished Record

One at-fault accident or a serious ticket can wipe out years of good-driver savings in an instant. To an insurer, these events are major red flags that signal a higher chance of a future claim. The financial hit is immediate and significant.

Real-World Impact: In Fort Lauderdale, a single at-fault accident can make your premium skyrocket. For instance, State Farm’s median annual rate can jump to around $3,927 after one incident. A DUI is even more severe, potentially pushing that same premium past $4,500.

These aren't small adjustments. They're major financial penalties that can follow you for several years.

Taking Control of Your Driving Profile

Here's the most important part: your driving profile isn't set in stone. You have a ton of control over it. By being proactive, you can actively build a profile that insurers see as low-risk, unlocking much better rates.

Here are a few moves you can make right now:

- Complete a Defensive Driving Course: This is low-hanging fruit. Many insurers offer a discount for finishing an approved course. It’s a small time investment that proves you're serious about safety.

- Check Your Driving Record: Pull a copy of your motor vehicle record (MVR) every so often to make sure it’s accurate. Mistakes can and do happen, and you don’t want to be paying for an error that isn't yours.

- Know Your Timelines: Most violations and accidents will affect your rates for three to five years. Mark your calendar. The moment an old incident "falls off" your record is the perfect time to shop for new insurance quotes.

When you manage these details, you're not just crossing your fingers for lower premiums—you're actively earning them. A clean profile is your single most powerful tool for finding affordable coverage.

Unlocking Every Available Car Insurance Discount

Finding affordable auto insurance in Fort Lauderdale isn't just about grabbing the lowest base price you see online. The real secret to slashing your premium lies in the discounts—and there are way more of them than most people think.

Too many drivers assume their insurance company is automatically giving them every break they qualify for. Big mistake. Insurers won't always hand them over unless you specifically ask. Think of it like a game where you have to know the cheat codes to win.

Go Beyond the Obvious Savings

Everyone knows about the "good driver" discount. That’s the low-hanging fruit. But if you stop there, you're leaving serious cash on the table. Insurers have a whole menu of discounts tied to your car, your lifestyle, and even how you prefer to pay your bill.

Getting granular here is what separates a decent rate from a great one. Let's dig into some of the most impactful (and often missed) categories.

-

Vehicle-Based Discounts: Is your car loaded with safety gear? Features like anti-lock brakes, multiple airbags, and anti-theft systems are all potential money-savers. Some companies even offer a small price cut for having daytime running lights.

-

Policy-Related Discounts: This is where you can find some of the biggest wins. Bundling your auto policy with home or renters insurance is the classic move, but don’t stop there. You can often score savings for paying your entire premium upfront, setting up automatic payments, or opting for paperless statements.

-

Driver-Based Discounts: Your personal profile is a goldmine for savings. The good student discount is a must-have for young drivers with good grades. But did you know you might qualify for a discount just by being a member of a professional group (like for teachers or engineers) or an alumni association?

Never dismiss a discount as "too small." A 3% savings here and a 5% savings there can add up quickly, making a real dent in your monthly payment.

Your Fort Lauderdale Auto Insurance Discount Checklist

To make sure you don't miss a thing, use this checklist as your guide when you're talking to an agent or getting quotes. It covers the most common discounts available to drivers right here in Fort Lauderdale.

| Discount Category | Specific Discounts to Ask For | Who Typically Qualifies |

|---|---|---|

| Policy & Loyalty | Multi-Policy (Bundling), Multi-Car, Loyalty/Renewal, Pay-in-Full, Auto-Pay, Paperless Billing | Homeowners, renters, families with multiple vehicles, and long-term customers. |

| Driver Profile | Good Student, Defensive Driving Course, Professional/Affinity Group (e.g., alumni, military) | Students with a "B" average or better, drivers who complete an approved course, and members of specific organizations. |

| Vehicle Safety | Anti-Theft System, Anti-Lock Brakes (ABS), Airbags, Passive Restraint Systems, New Car Discount | Owners of vehicles with standard or advanced safety and security features, or a recently purchased car. |

This simple list can be a powerful tool. By proactively asking about each one, you put yourself in the driver's seat of the negotiation.

Pro Tip: Before you start calling for quotes, make a list of your car's specific safety features. When you explicitly mention things like your anti-theft system or side-curtain airbags, it forces the agent to check for discounts they might otherwise overlook. It's a direct path to a better rate.

This proactive approach is everything. When you treat discounts as a critical part of the conversation, you take control of your premium. For even more ways to trim your bill, our guide on how to lower car insurance costs has other practical strategies you can use today. A few extra minutes of diligence here will pay off every single month.

A Smarter Way to Compare Insurance Quotes

Getting a handful of car insurance quotes is a great first step, but it’s only half the battle. The lowest number you see isn't automatically the best deal. Real savings come from knowing how to dissect those quotes and make a smart, apples-to-apples comparison.

This is how you move past just chasing a cheap premium and find the best overall value for your actual needs here in Fort Lauderdale. Without a solid method, you could easily pick a policy that looks good upfront but has coverage gaps that will cost you big time down the road.

Get Your Ducks in a Row First

Before you even start shopping, pull all your information together. Seriously, this makes the process so much faster and ensures every insurer is quoting you based on the exact same data. This is the bedrock of an accurate comparison.

Have these details ready to go:

- Driver Info: Full names, dates of birth, and driver’s license numbers for everyone you plan to put on the policy.

- Vehicle Details: The Vehicle Identification Number (VIN), make, model, year, and current mileage for each car.

- Driving History: Be ready to share any accidents, tickets, or claims within the last five years for all drivers.

- Your Current Policy: Grab your existing declarations page. It shows your current coverage limits and what you’re paying right now.

Having this stuff prepared eliminates guesswork and keeps the quotes consistent, which is absolutely critical for a fair evaluation.

Compare More Than Just the Price Tag

The single biggest mistake I see drivers make is focusing only on the final premium. A cheap quote is worthless if it doesn't give you the protection you actually need. To find cheap auto insurance in Fort Lauderdale that’s also good insurance, you have to line up the core components of each quote side-by-side.

Pay close attention to these three areas:

- Coverage Limits: Make sure the liability limits (for example, $100,000/$300,000/$50,000) are identical on every single quote. A policy with lower limits will always be cheaper, but it leaves you dangerously exposed if you cause a serious accident.

- Deductibles: Your deductible for comprehensive and collision coverage directly swings your premium up or down. Ensure you're comparing quotes with the same deductible—whether it's $500 or $1,000—to see the true price difference.

- The Extras: Does one quote include rental car reimbursement or roadside assistance while another doesn't? These add-ons provide real value and should absolutely be factored into your decision.

By making sure these variables are the same across the board, you stop looking at just the price and start comparing the actual value each company brings to the table. It’s the only way to be certain you're not sacrificing critical protection for a slightly lower monthly payment.

It also helps to understand how different carriers operate across South Florida. For instance, digging into the variety of insurance companies in Miami, Florida can reveal regional trends and provider strengths that are often just as relevant here in Fort Lauderdale. This wider perspective helps you make a more informed choice, ensuring you partner with a company that truly gets the local landscape.

Unpacking Fort Lauderdale’s Top Car Insurance Questions

When you're trying to lock in the best car insurance deal in a place like Fort Lauderdale, a lot of questions pop up. It's a busy area with unique risks, and getting straight answers is the first step to saving money. Let's tackle some of the most common things drivers ask.

A big one is always about traffic tickets. Will one little slip-up send your rates through the roof? It really depends. A minor speeding ticket might just give your premium a small nudge, but a citation for something serious like reckless driving or a DUI? That’s going to have a much bigger, longer-lasting impact on your ability to find cheap auto insurance.

Does My Credit Score Really Matter?

Yes. 100%. In Florida, insurers are legally allowed to use a credit-based insurance score when they calculate your premium.

Why? The data shows a strong link between a person's credit history and how likely they are to file a claim. To an insurer, a good credit score suggests you're financially responsible, and they often reward that with a lower, more affordable rate. Think of improving your credit as a long-term strategy for cheaper insurance.

Another question we hear all the time is about adding new drivers, especially teenagers. If you have a teen driver living in your house, they absolutely must be added to your policy. Trying to exclude them isn't an option and is a surefire way to get a claim denied.

Yes, adding a young driver is expensive, but you can soften the blow. Make sure you're getting every discount they qualify for, like the good student discount.

Key Insight: The company that gave you the best rate as a solo driver might not be the most affordable once you add a teenager. This is a critical moment to shop around and compare quotes all over again—don't just accept the new price from your current insurer.

What If I Drive for Uber or Lyft?

This is a huge one. Your standard personal auto policy almost certainly does not cover you while you're driving for a rideshare service.

To be properly protected, you'll need a specific rideshare insurance policy or, at the very least, an endorsement added to your personal policy. Driving without it creates a massive coverage gap that could leave you on the hook for thousands after an accident.

People also wonder if they're stuck with the big national brands. What about other options, like the insurance programs offered by warehouse clubs? It's always smart to understand the details. For example, you can dive into how programs like Costco's car insurance availability in Florida work to see if they're a good fit. Getting answers to these kinds of questions is what helps you make a truly informed decision.

Ready to get clear answers for your specific situation and find the best possible rate? The experts at MyEasyRate Insurance are here to help you compare quotes from top carriers and build a policy that fits your life and your budget. Visit https://myeasyrate.com to get your free, no-obligation quote today.

Article created using Outrank