For a business owner, disability insurance isn't just a personal safety net. It's a core business continuity strategy. This coverage protects your single most valuable asset—your ability to earn an income—making sure an unexpected illness or injury doesn't sink both your personal finances and your company.

Why Your Ability to Work Is Your Biggest Asset

Let's be honest. For most entrepreneurs, the business itself—the office, the inventory, the brand—isn't the main asset. Your real value is your brain, your drive, and your daily hustle.

Think of your business like a high-performance car. It has all the right parts in place: employees, clients, and a great product. But you are the engine. If that engine suddenly shuts down, the whole operation grinds to a halt.

A serious disability doesn't just stop your paycheck. It directly threatens your company's survival by stalling projects, disrupting operations, and rattling the confidence of your customers and employees. This is where disability insurance for business owners steps in, acting as a financial backstop that keeps the lights on while you focus on recovery.

The Unique Risks of Being the Boss

Unlike a traditional employee who might get sick pay or have a team to cover for them, business owners face a completely different set of dangers. Your personal financial health is welded to your company's stability. A long absence can quickly unravel everything you’ve poured your life into building.

For an entrepreneur, a personal disability is a business crisis. The fallout goes way beyond one missed paycheck—it hits payroll, rent, and the long-term health of the entire company.

The risks you carry are simply on another level, and they demand a much stronger and more specific type of protection than a standard employee policy can offer.

Business Owner vs Employee Disability Risks at a Glance

When a disability strikes, the financial shockwaves hit a business owner and a traditional employee in vastly different ways. Here’s a quick breakdown of where the pressure points are.

| Risk Area | Impact on a Business Owner | Impact on a Traditional Employee |

|---|---|---|

| Income Source | Solely responsible for generating revenue; income stops immediately. | Receives sick leave or worker's comp; income is partially protected. |

| Business Operations | Key decisions halt; projects stall, and management is disrupted. | Duties are delegated to colleagues or temporary staff. |

| Fixed Costs | Personally liable for rent, payroll, and utilities, even with no income. | No direct responsibility for the company’s overhead expenses. |

| Client Relationships | Direct relationships may falter, leading to lost business. | The company manages client continuity through the team. |

As you can see, the stakes are far higher when you're the one in charge. While an employee's main concern is their personal paycheck, a business owner has to worry about that plus keeping the entire company afloat.

Decoding Your Disability Insurance Policy

To get the right disability insurance for business owners, you have to know how to read the fine print. Cutting through the industry jargon is the first and most important step toward making a smart decision that actually protects your income and your company.

Let's break down the core components you’ll find in any policy. Think of this as the user manual for your financial safety net.

Own-Occupation vs. Any-Occupation Coverage

This is, without a doubt, the most critical detail in any disability policy, especially for a skilled business owner. The definition of "disability" is what determines whether—and when—you actually get paid.

- Own-Occupation: This coverage considers you disabled if you can no longer perform the main duties of your specific job. For an entrepreneur, this is almost always the best-case scenario.

- Any-Occupation: This is much tougher. It only considers you disabled if you can’t perform the duties of any job for which you are reasonably suited by your education and experience.

Here’s a real-world example. Imagine a surgeon who develops a tremor in her hands. Under an own-occupation policy, she's disabled. She can no longer perform surgery, so her benefits would kick in, even if she could pivot to teaching or consulting.

But with an any-occupation policy? The insurance company could argue she isn't truly disabled because she can still earn a living as a medical consultant. The difference is huge.

The definition of disability is the heart of your policy. For specialized entrepreneurs, "own-occupation" coverage provides the strongest protection by recognizing the unique value of the specific work you do.

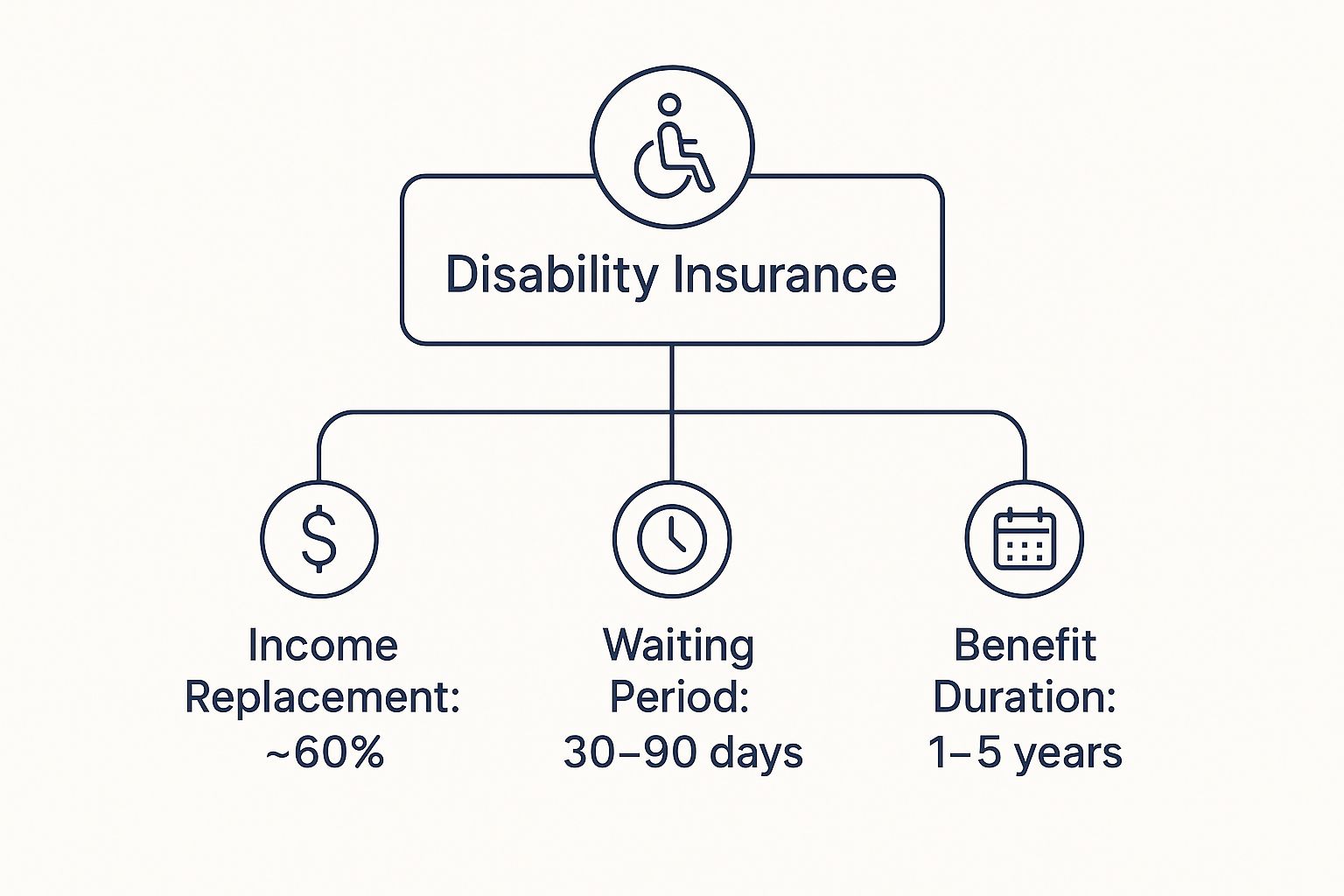

The Waiting and Payment Timelines

Every policy has two key timelines that dictate when your payments start and how long they last. Getting these right is crucial for managing your cash flow if a crisis hits.

First up is the elimination period, which is just another name for the waiting period. Think of it like a deductible, but measured in time instead of dollars. It’s the number of days you must be disabled before your benefits begin, typically ranging from 30 to 180 days. Choosing a longer waiting period will usually get you a lower premium.

Next is the benefit period. This defines how long you can receive your monthly payments once they start. It might be a set number of years—like two, five, or ten—or it could last all the way to a specific age, like 65 or 67. The benefit period you select directly impacts both your premium cost and, more importantly, your long-term financial security.

The Three Policies Every Business Owner Should Know

If you’re a business owner, your ability to work is the business. A standard personal disability policy is great for replacing your own paycheck, but what happens to the company itself if you’re suddenly unable to run it?

That personal policy won’t cover rent, make payroll, or handle the chaos left in your absence. This is exactly why a different kind of protection exists: disability insurance for business owners. Let's break down the three essential policies designed to keep your company afloat, your partners protected, and your legacy secure.

This is a quick look at the core components you'll find in most disability policies. It's a handy reference for the terms we're about to cover.

As you can see, the basic idea is to replace a chunk of your income—usually around 60%—after a waiting period, with benefits that last for a set number of years. But for a business, that's just the start.

Business Overhead Expense (BOE) Insurance

Think of Business Overhead Expense (BOE) insurance as a lifeline that keeps the lights on when you can’t be there. If a disability takes you out of the game temporarily, this policy steps in to pay for all the fixed, day-to-day costs of running the business.

BOE is designed specifically to cover recurring bills so the company doesn't bleed cash while you recover. It typically pays for things like:

- Rent or mortgage on your office or storefront

- Employee salaries and payroll taxes

- Utilities like electricity, water, and internet

- Property taxes and business insurance premiums

Crucially, this policy doesn't pay your salary. Its only job is to cover the essential overhead that keeps the business viable. This is especially important in states with strict rules around employee coverage. For more on that, our guide on workers' compensation in Florida gives some helpful context on related employer duties.

Key Person Disability Insurance

What would happen if your lead software developer, your top rainmaking salesperson, or your visionary head chef suddenly couldn't work for a year? For many companies, losing that one indispensable employee would be catastrophic.

Key Person Disability Insurance is the answer. It’s a policy the business owns on a crucial employee. If that person suffers a disability, the company receives the payout.

The funds give you breathing room and options. You can use the money to:

- Hire and train a top-tier replacement.

- Make up for lost revenue while projects are on hold.

- Reassure investors that the company is stable.

This policy acts as a financial shock absorber, ensuring the disability of one critical person doesn't sink the entire ship.

Disability Buy-Out Insurance

For businesses with multiple partners, the long-term disability of one owner can create a messy, emotional, and financially devastating situation. A Disability Buy-Out policy is designed to prevent that exact scenario.

This policy provides the cash needed to smoothly execute a buy-sell agreement you’ve already put in place.

It's a clean solution. The disabled partner gets a fair price for their share of the business, and the remaining partners get to keep control without having to drain their personal savings or company cash reserves to buy them out.

Taking this step ahead of time prevents painful negotiations, financial strain, and potential lawsuits down the road. It's a proactive move gaining traction fast; sales of these business-specific disability products have climbed about 8% annually over the last five years as more owners realize just how exposed they are.

What Really Determines Your Insurance Premium

Ever wondered how an insurance company lands on your specific premium? It might seem like they’re just picking numbers out of a hat, but there’s a clear logic behind it. They’re simply calculating the odds that you’ll actually need to file a claim.

When you understand the moving parts, you can make smarter decisions and build a policy that gives you solid protection without breaking the bank. Your premium for disability insurance for business owners boils down to two big things: your personal risk profile and the specific coverage choices you make.

Your Personal Risk Profile

First things first, the insurance carrier looks at you. It’s all about risk assessment, and these personal details form the foundation of your premium.

- Age and Health: This one’s pretty straightforward. Younger and healthier people get better rates because, statistically, they're less likely to become disabled. Any pre-existing conditions or a history of illness can nudge your premium higher.

- Occupation: Your job is a huge factor. A software developer working from a home office is going to pay a lot less than a general contractor who’s on-site every day. It all comes down to the physical risks of your profession.

- Hobbies and Habits: What you do for fun matters, too. If you’re into high-risk hobbies like scuba diving or if you’re a smoker, carriers see that as an increased statistical chance of injury or illness, which will be reflected in your rate.

These factors give the insurer a baseline snapshot of your individual risk. From there, it’s all about how you customize the policy itself.

At its core, an insurance premium is the price you pay to transfer risk. The more risk the insurer takes on—whether from your job, your health, or your policy choices—the higher that price will be.

How Your Policy Choices Adjust the Price

This is where you’re in the driver’s seat. By tweaking the features of your policy, you can directly influence your monthly cost. It’s a bit like customizing a new car—upgraded features cost more, while standard options keep the price down. The trick is to find the perfect balance between the coverage you need and what your business can comfortably afford.

Here's a simple breakdown of how different policy levers can raise or lower your costs.

How Policy Choices Impact Your Premium

This table shows how adjusting key features can directly impact what you pay each month.

| Policy Feature | Example Choice A (Lower Cost) | Example Choice B (Higher Cost) | Impact on Premium |

|---|---|---|---|

| Elimination Period | A 180-day waiting period | A 30-day waiting period | A shorter wait for benefits significantly increases the premium. |

| Benefit Period | Payments for up to 5 years | Payments until age 67 | Longer-lasting benefits offer more security but come at a higher cost. |

| Benefit Amount | $5,000 per month | $10,000 per month | A higher monthly payout directly corresponds to a higher premium. |

As you can see, a policy with a longer waiting period, a shorter benefit timeline, and a lower monthly payout will be much more budget-friendly. The key is to run the numbers for your own situation and decide which trade-offs make the most sense.

Why Income Protection Is More Critical Than Ever

If you still think of disability insurance as a dusty "worst-case scenario" plan, it's time for a reality check. For today’s entrepreneurs, it's a core strategic tool. Your personal income and your business's health are tied together at the hip, making income protection less of an option and more of a necessity.

The financial ground has shifted under our feet. Old safety nets are fraying while medical bills just keep climbing. That's a high-stakes gamble for anyone, but for a business owner with a fluctuating income and bills that never stop, the risk is dialed up to eleven.

The New Economic Reality for Entrepreneurs

Relying on your savings to get you through a long-term disability is a bigger gamble than ever before. A sudden illness or injury doesn't just cut off your paycheck; it puts your entire business on life support. Without you steering the ship, revenue can evaporate, but fixed costs like rent, payroll, and supplier bills keep coming.

This isn't just a hunch; the market shows a clear trend. The global disability insurance market, valued at $4.11 billion in 2024, is on track to hit $7.11 billion by 2029. That kind of growth tells a story: more and more business owners are waking up to the fact that this coverage isn't just nice to have—it's essential.

Getting income protection isn't about being pessimistic. It's a smart financial move, driven by the clear reality that trying to self-fund a long-term disability is an increasingly impossible risk for a modern business owner.

Protecting More Than Just a Paycheck

For an entrepreneur, a disability policy does so much more than just replace a salary. It builds a firewall between a personal health crisis and a business-ending financial disaster. It gives you the stability to pay your mortgage and groceries without gutting your business accounts or racking up high-interest debt just to stay afloat.

Think about it this way: other policies protect your business's stuff—your equipment, your building, your inventory. But disability insurance for business owners protects the one thing that makes it all run: you.

Sure, general liability insurance matters for protecting against third-party claims, but it won't pay you a dime if you're too sick to work. This is about insuring the pilot, not just the plane.

Finding the Right Disability Coverage for Your Business

Knowing you need disability insurance is one thing. Actually putting a rock-solid plan in place is what truly protects your life’s work. This isn’t about just buying a policy; it's about building a layered defense that fits your specific financial world. It all starts with a no-nonsense needs analysis.

First, you need to calculate exactly what you’re protecting. Add up your non-negotiable personal monthly bills—mortgage, groceries, car payments, utilities—to figure out your income replacement target. Then, on a separate sheet, list your essential business overhead: rent, payroll, key software, and loan payments. These two numbers are the foundation of your entire strategy.

Partnering with the Right Professional

Once you have your numbers, resist the urge to call a generalist. You need an independent insurance professional who lives and breathes this stuff for business owners. Their expertise is critical because they get the nuances of policies like Business Overhead Expense (BOE) and know how to navigate the underwriting process for entrepreneurs. This isn't a niche concern anymore—coverage among self-employed workers hit 29% in 2023. You can dig into these trends and discover key disability insurance statistics on coinlaw.io.

A true expert helps you build a strategy that shields both your family’s kitchen table and your company’s future. Think of it this way: you wouldn't use the same insurance for your office building as you would for your work truck. The same logic applies here. For instance, if your business relies on specialized gear, our guide on what insurance you need for a trailer shows just how different asset protection can be.

Your advisor’s primary role is to translate your business realities into a resilient insurance strategy. They should act as a strategic partner, not just a salesperson.

To make sure you find the right fit, show up to the conversation with sharp questions. A great advisor will welcome them.

- How many of your clients are business owners in my industry?

- Can you explain the key differences between "own-occupation" riders from various carriers?

- How should we structure these policies to align with our buy-sell agreement?

Asking questions like these turns a simple transaction into a strategic partnership, making sure the plan you build today is the one that will actually be there for you tomorrow.

Common Questions from Business Owners

Even with a solid plan, a few key questions always pop up when entrepreneurs start digging into disability insurance. Let's tackle the most common ones we hear, connecting the big ideas to the real-world decisions you'll have to make.

Are My Disability Insurance Benefits Taxable?

This is a huge one, and the answer comes down to a simple trade-off: who pays the premium? The IRS gets its share one way or another, either on the money going in (premiums) or the money coming out (benefits).

-

You Pay With Personal, After-Tax Dollars: If you pay for your own disability policy with your own money that's already been taxed, any benefits you receive down the road are typically tax-free. This is the most common setup for individual policies.

-

Your Business Pays and Deducts the Premium: If your company pays for a policy (like Business Overhead Expense insurance) and writes it off as a business expense, the benefits are considered taxable income. This makes sense because the benefits are designed to pay for other deductible business expenses like rent, utilities, and payroll.

Can I Get Coverage If My Business Is Brand New?

Yes, absolutely. But insurers will want to kick the tires a bit more. Since a new venture doesn't have years of profit-and-loss statements to show, carriers will look closely at your business plan, your financial projections, and your own professional track record.

Some insurers even have policies built for startups. They'll let you start with a modest amount of coverage and then increase it as your income grows, often without needing to go through a whole new medical exam. This is exactly where a specialist who knows the market can make all the difference.

For a startup, disability insurance isn't just about replacing a paycheck. It's about protecting your initial investment and giving your dream a fighting chance to survive if you're suddenly sidelined.

Do I Really Need Both Personal and Business Insurance?

For almost every business owner, the answer is a firm "yes." The two policies are designed to protect completely different things, and one simply can't do the job of the other.

Think of it this way: your personal disability policy is there to keep your life at home running. It pays your mortgage, buys the groceries, and protects your family’s financial world.

Your Business Overhead Expense insurance, on the other hand, protects your company. It pays the office rent, covers employee salaries, and keeps the lights on so there's a business to come back to. One protects your household, the other protects your livelihood.

Ready to build a strategy that protects both your family and your business? The team at MyEasyRate Insurance specializes in helping entrepreneurs find the right mix of coverage. Get your free, no-obligation quote today!